Spinouts have defied the slump in the rest of the market, with deal numbers up 10% from last year. The average size of seed and series B rounds has actually increased.

The market may have cooled elsewhere, but spinouts enjoyed their best quarter for fundraising in Q3 — with the number of deals up more than 10% from the same quarter last year.

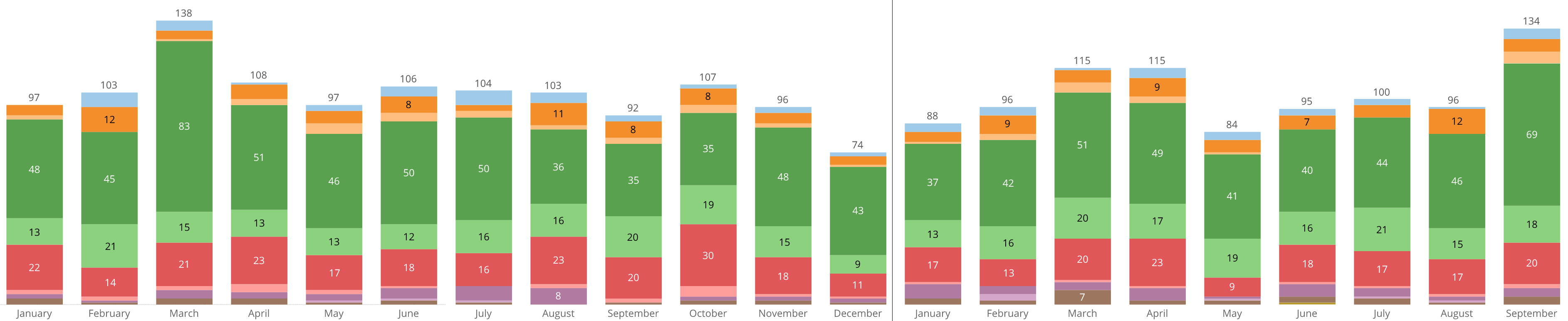

There were 330 investments in spinouts in the third quarter of 2022. That is up from 294 in the second quarter of this year and, more notably, up year-on-year from 299. It’s also the best quarter of the year so far, with the first quarter having seen 299 investments.

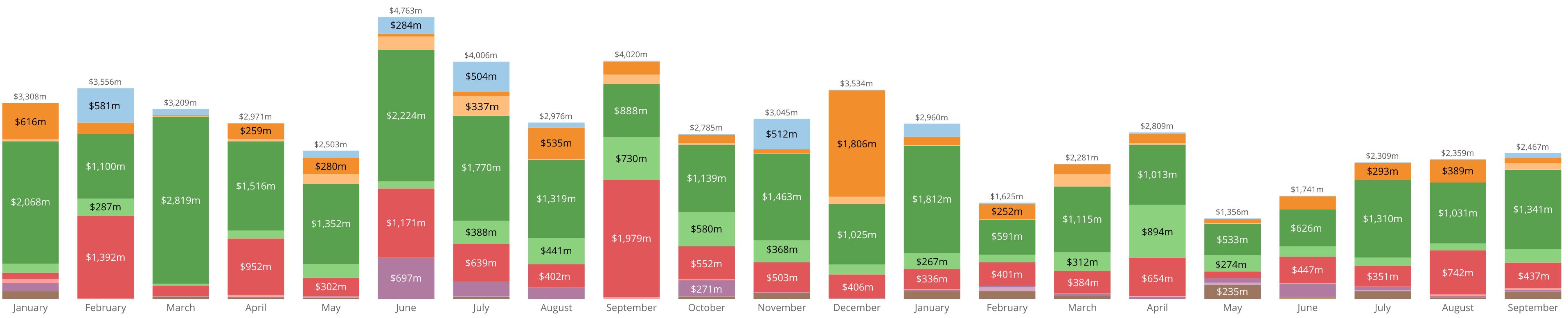

It is a case of less money going into more deals, however. The amount of capital going into deals fell to $7.1bn in Q3, compared to $11bn in the same period last year, when July and September saw more than $4bn invested. But the Q3 amount is showing an upward trend, from $6.8bn in the first quarter and $5.9bn invested in Q2.

The rise in deal numbers may be modest, but it is remarkable that this group of startups is bucking the general slump. A recent analysis by Global Corporate Venturing found that CVC-backed deals fell 11% quarter-on-quarter and more than 16% year-on-year.

It could be a sign that investors subscribe to the theory that spinouts are a safer bet than startups more generally and become particularly attractive when venture capital is in a slump. Research by law firm Anderson Law in 2019 found that nine out of 10 spinouts in the UK survive longer than five years, compared with just two out of 10 of other startups.

Investments from January 2021 to September 2022

It is also interesting to note that healthcare made up a larger percentage of deals in Q3 2022 than in 2021: 48.2% (159 deals) compared to 40.5% (121 deals). Some of these are obvious technologies — they range from cancer diagnostics to remote patient monitoring platforms — others are more futuristic-sounding, such as ForSight Robotics, linked to Technion – Israel Institute of Technology, which is developing a platform for fully robotic cataract surgery and raised $55m in its series A round led by Adani in July.

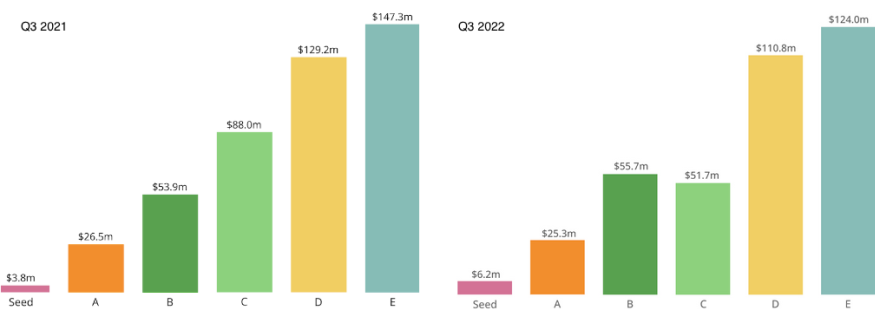

ForSight’s raise was large for series A. In general, the average size of these rounds decreased year-on-year from an average $26.5m to $25.3m.

The average seed round, however, was worth considerably more in the third quarter of 2022 than 2021: $6.2m versus $3.8m, and just as notably more than the average for any quarter in 2021. This may not be a surprise given that early-stage companies have been the last to feel the funding chill. But surprisingly series B rounds were also up, from $53.9m to $55.7m.

Average round size in Q3 2021 and Q3 2022

It suggests investors have identified a sweet spot that they hope will serve them through the slump: in a series B the technology is sufficiently de-risked with a growing customer base, but valuations are still manageable. Although it should be noted that out of the top 10 biggest deals in the past quarter, three were series B rounds with hefty amounts: $225m for Delfi Diagnostics, $221m for Orna Therapeutics and $220m for Arsenal Biosciences.

Series C rounds, on the other hand, have suffered the most. Series D and E rounds have also suffered, albeit not as much.

Top 10 investments in Q3 2022

| Company | University | Country | Sector | Round | Size |

|---|---|---|---|---|---|

| Celonis | TU Munich | Germany | Services | D (extension) | $400m |

| SeatGeek | Stanford University | US | Services | E | $228m |

| Delfi Diagnostics | Johns Hopkins University | US | Healthcare | B | $225m |

| Orna Therapeutics | Massachusetts Institute of Technology | US | Healthcare | B | $221m |

| Arsenal Biosciences | University of California, San Francisco | US | Healthcare | B | $220m |

| Nexeon | Imperial College London | UK | Cleantech | Undisclosed | $200m |

| Cleerly | Cornell University, NewYork-Presbyterian Hospital | US | Healthcare | C | $192m |

| Cera | Vanderbilt University’s Endowment | UK | Healthcare | Undisclosed | $160m |

| Fervo Energy | University of California (Congruent Ventures) | US | Energy | Undisclosed | $138m |

| SOURCE Global | Arizona State University | US | Consumer | D | $130m |

Exits from January 2021 to September 2022

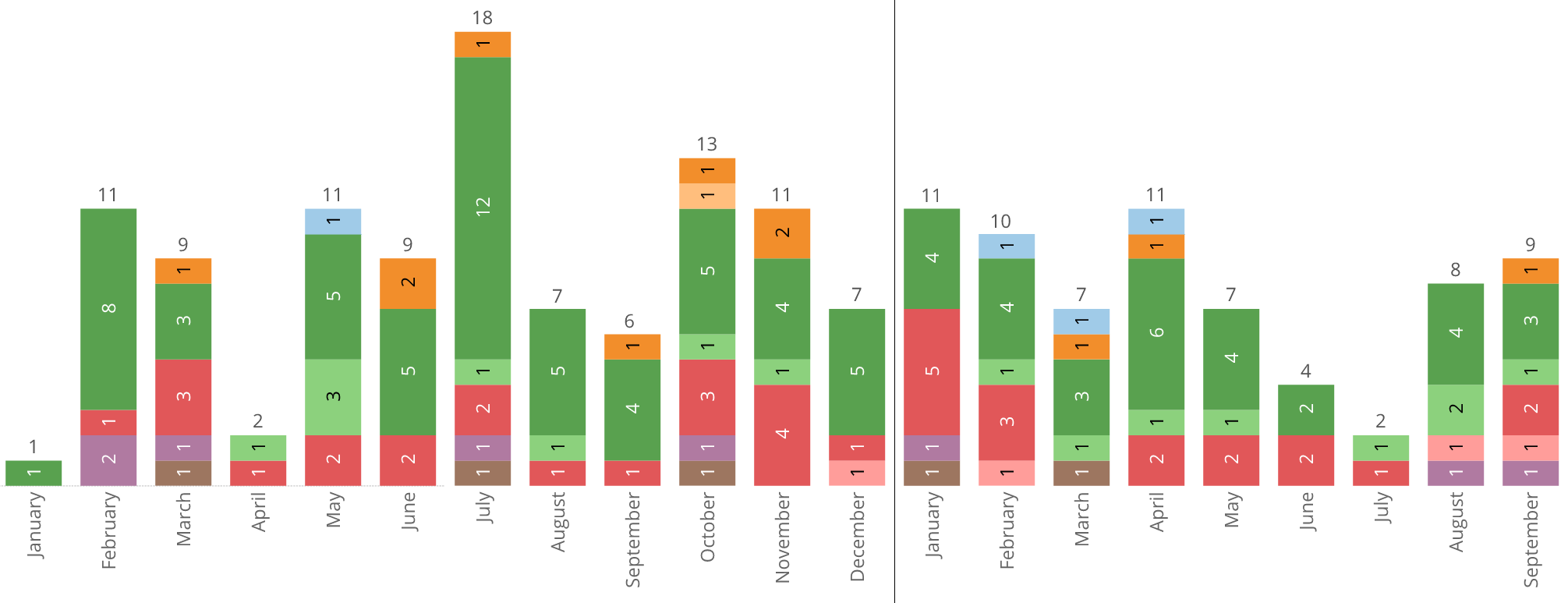

It’s a bleaker picture when looking at exits. Just $738m were disclosed for 19 in the third quarter this year, compared with more than $2.5bn generated through 31 exits in the third quarter of 2021. It is a sobering fall, but spinouts are clearly suffering from the same lull in initial public offerings as the wider ecosystem.

There were, in fact, no traditional IPOs during the entire quarter. Reverse mergers are still happening, most notably perhaps that of Brown University’s Ocean Biomedical (focused on non-small cell lung cancer, malaria and pulmonary fibrosis), which announced its intention to go public by buying the special purpose acquisition corporation Aesther Healthcare Acquisition by December. It’s notable because Ocean Biomedical had actually planned to pursue the traditional IPO route, and had already filed a draft prospectus.

Small caveat on the table below: the merger was extended to be concluded by December and the amount has increased outside the quarter with another $40m backstop deal in early October.

Virtuoso Surgical, a minimally invasive endoscopic robotic surgery system developer co-founded by Johns Hopkins University and Vanderbilt University researchers, pursued a $20m stock offering in September but this occurred under the Securities and Exchange Commission’s Regulation A, Tier 2 — meaning Virtuoso was able to offer $20m worth of stock to investors without having to deal with the costly and lengthy process of a registration statement.

As is common, the majority of acquisitions were for undisclosed sums. Gilead paid $405m for University of Oxford’s autoimmune disease therapy developer MiroBio in August, making it the largest disclosed amount.

On the other hand, University College London’s ovarian cancer test spinout Abcodia was acquired for the unusual sum of $0 by predictive genetics company GENinCode. While there was no upfront consideration, there is a potential £1m ($1.2m) up for grabs on an earnout basis.

Top 10 exits in Q3 2022

| Company | University | Country | Sector | Type | Size |

|---|---|---|---|---|---|

| MiroBio | University of Oxford | UK | Healthcare | Acquisition | $405m |

| Carisma Therapeutics | University of Pennsylvania | US | Healthcare | Reverse merger | $180m |

| EmpowerTheUser | Trinity College Dublin | Ireland | Education | Acquisition | $50m |

| Ocean Biomedical | Brown University | US | Healthcare | Reverse merger | $40m |

| Flusso | University of Cambridge | UK | Industrial | Acquisition | $33.4m |

| Ducentis BioTherapeutics | LifeArc | UK | Healthcare | Acquisition | $30m |

| Virtuoso Surgical | Johns Hopkins University, Vanderbilt University |

US | Healthcare | IPO (Reg A) | $20m |

| Abcodia | University College London | UK | Healthcare | Acquisition | $0 |

| Oxford Ionics | University of Oxford | UK | IT | Acquisition | Undisclosed |

| RoadBotics | Carnegie Mellon University | US | Transport | Acquisition | Undisclosed |