The second quarter of 2024 has seen a boost in corporate exits, a rise in corporate seed stage investing, and an increase in deals in the media sector.

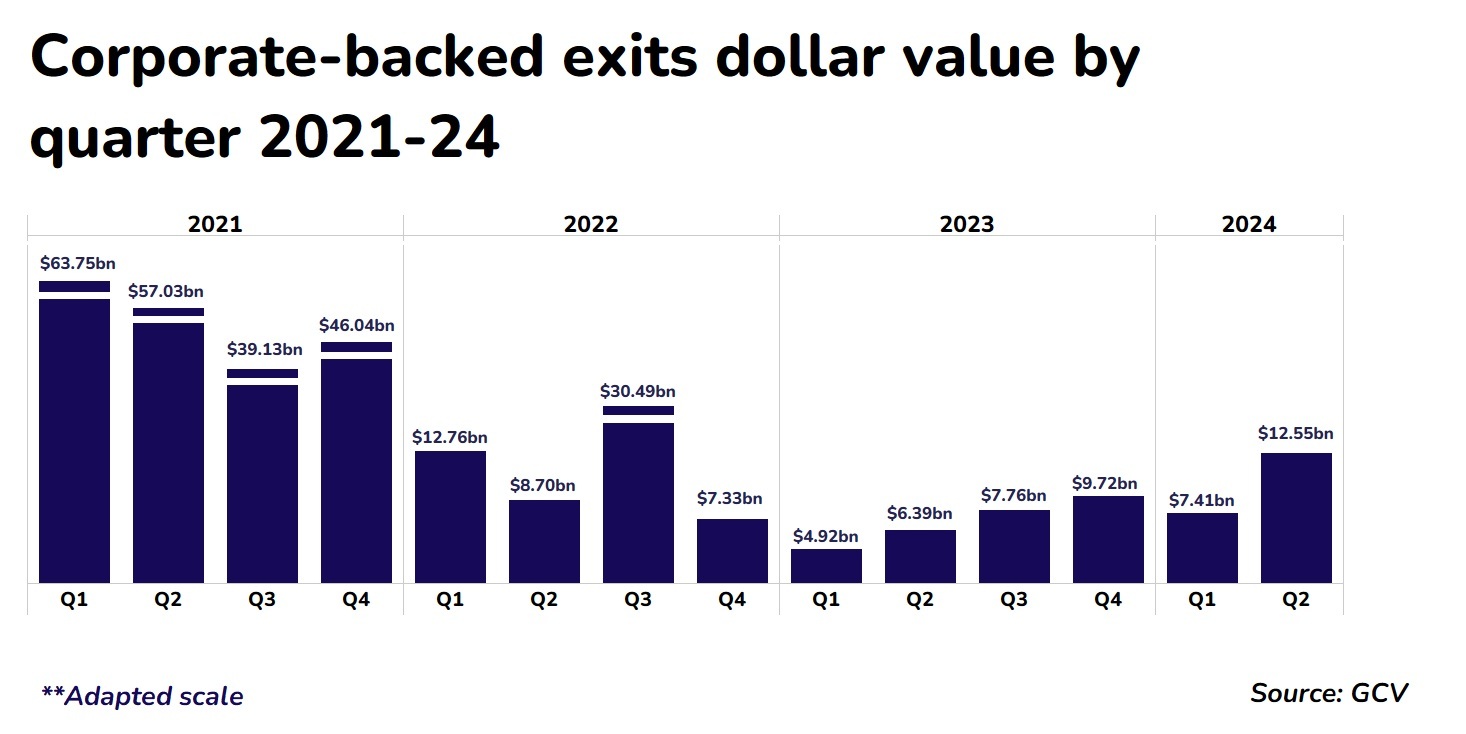

The second quarter of 2024 has seen a rise in exits for companies backed by corporate investors. The estimated dollar value of corporate-linked exits in Q2 2024 stood at $12.55bn – the highest it has been since the third quarter of 2022 when it was estimated $30.49bn, GCV data shows.

The dollar value of corporate-linked exits reached record levels in 2021 before seeing a dramatic fall in 2022. However, we have seen a gradual rise since the beginning of 2023. The nearly 70% quarter-on-quarter rise in the value of corporate-linked exits in Q2 this year is further evidence that the market is recovering from the post-covid dip.

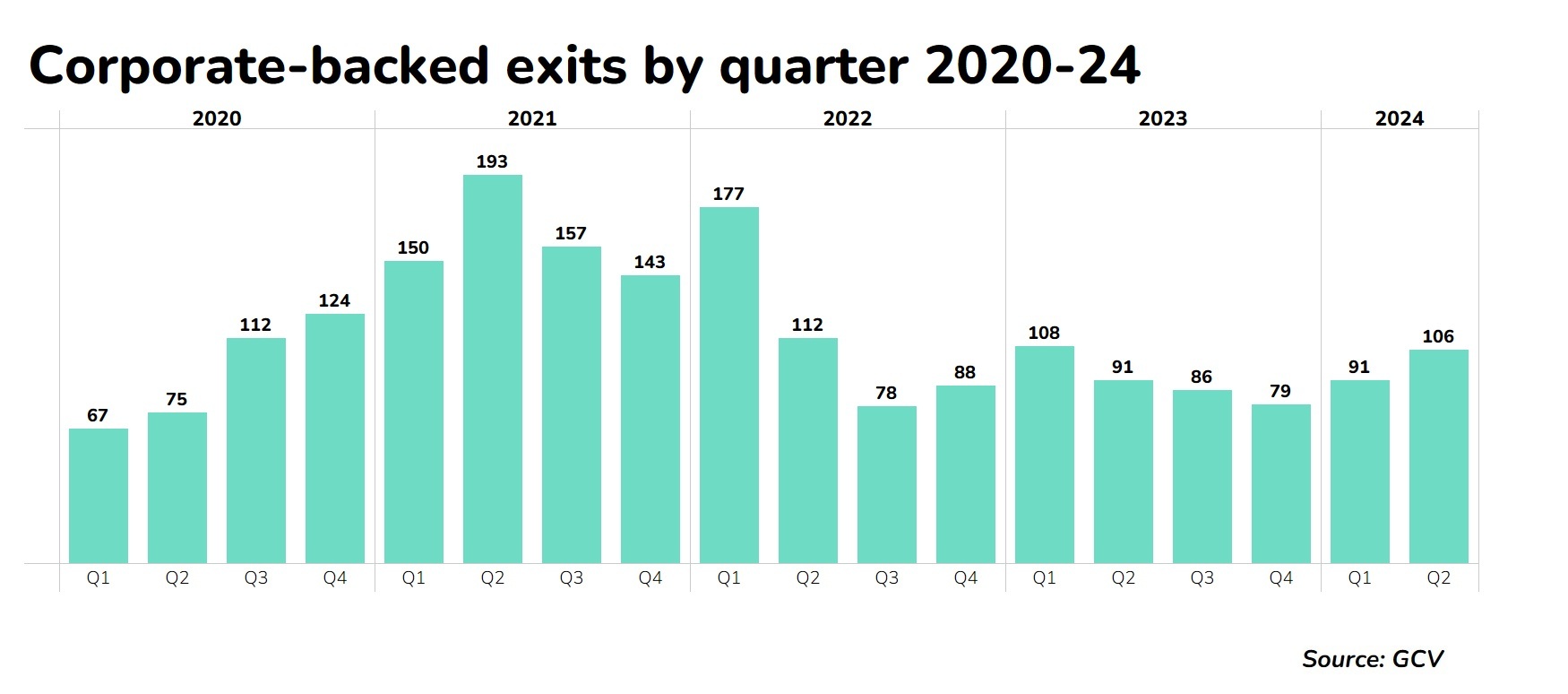

Corporate-linked exits have been increasing not just by value but also in number, although the pattern is much more mixed and it may be still too early to call this full-blown recovery phase.

In Q2 2024, there were four corporate-linked exits with values of more than $1bn, three of which were in the health sector.

The biggest exit of Q2 was cancer drug developer ProfoundBio, which was acquired for $1.8bn by Danish biotech company Genmab. ProfoundBio’s backers included drugs company Eli Lilly. The third largest exit of the quarter was MSD’s acquisition of ophthalmology biotechnology company EyeBio for $1.3bn, which it had previously invested in as a minority shareholder.

Other notable exits included Biogen’s $1.15bn acquisition of biotech Human Immunology Biosciences which develops treatments for immune mediated inflammatory diseases. German biopharmaceutical company MorphoSys had invested in the company.

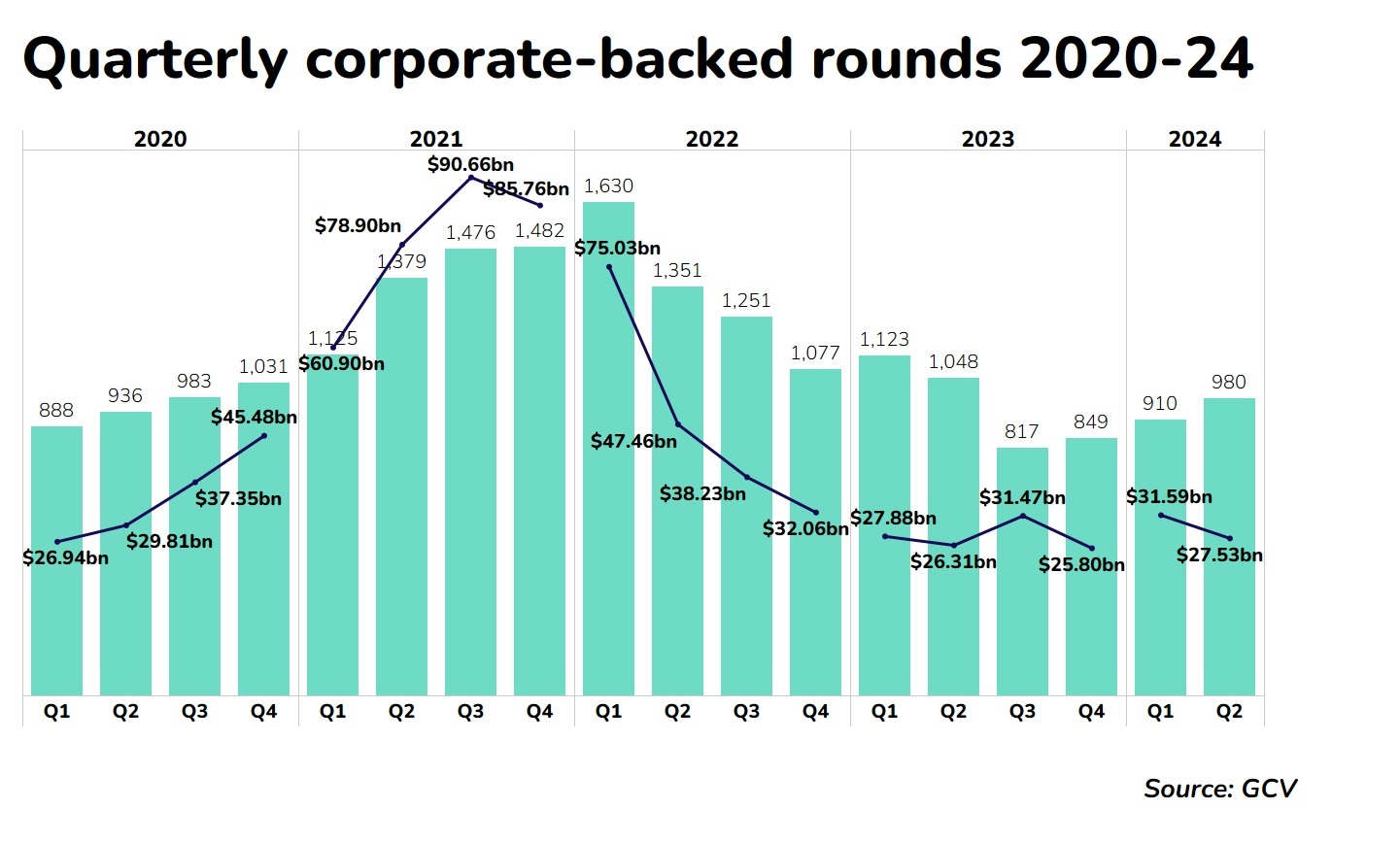

Corporate-backed funding rounds continue to creep up

The number of corporate-backed startup funding rounds continued to creep upwards, with the number increasing to 980 up from last quarter’s 910. While down versus the same period in 2023 (with 1048 rounds), the number of deals has been on the increase since Q3 last year.

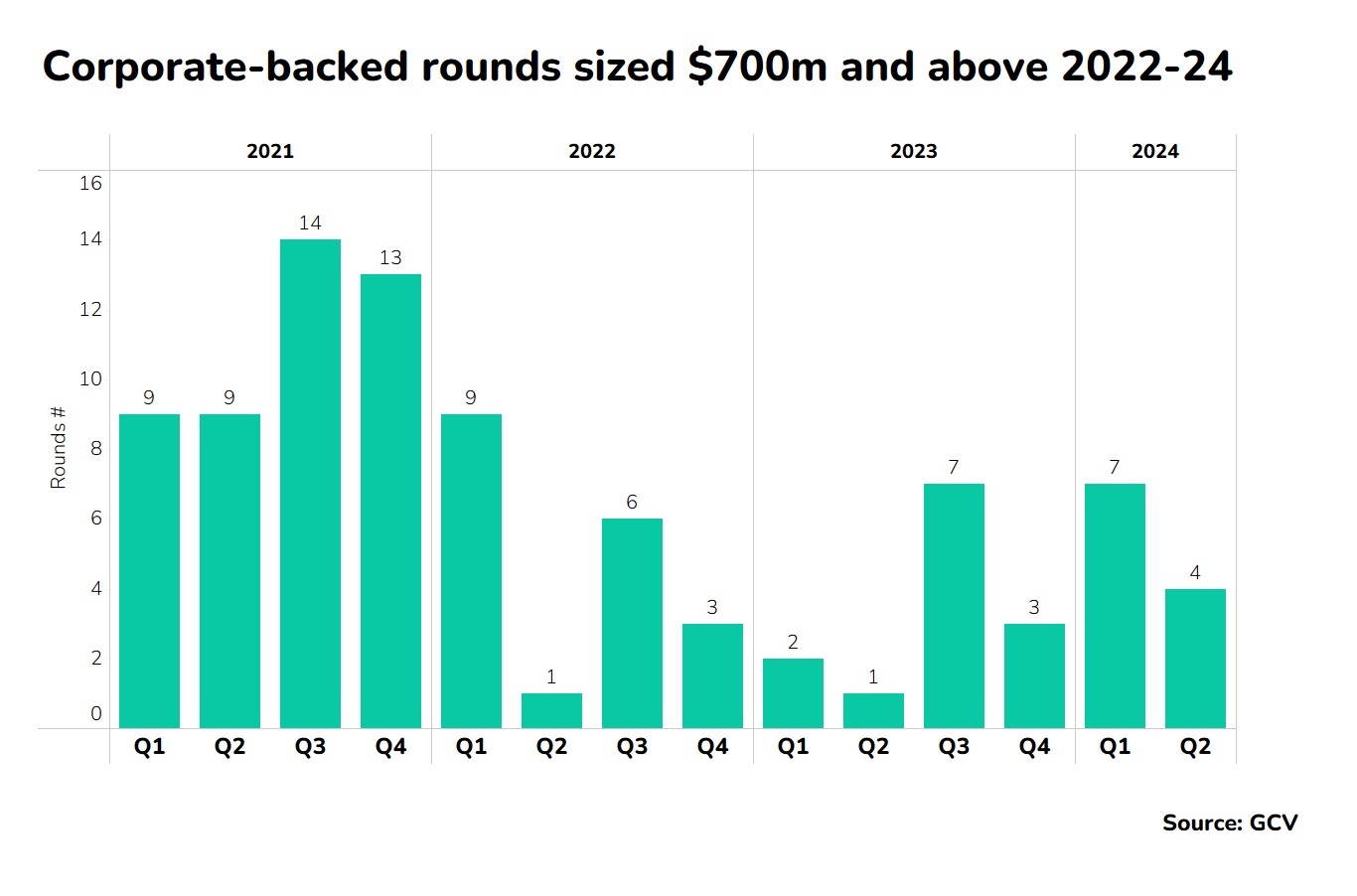

This quarter saw some bumper corporate-backed funding rounds, too. There were four rounds that were valued at $700m or more, compared to just one in Q2 the previous year. Microsoft invested $1.5bn for a minority stake in Abu Dhabi-based artificial intelligence company G42. UK company Wayve, a self-driving car technology developer, raised $1.05bn for its series C round, backed by Nvidia, Microsoft and Softbank.

Wiz, a cloud security software startup, raised $1bn in series E funding backed by Salesforce. In another big artificial intelligence round, Scale AI, which is developing a data engine for training advanced AI models, raised $1bn in series F funding, backed by Nvidia, Cisco, DFJ Growth, Intel, ServiceNow, AMD, Amazon and Meta.

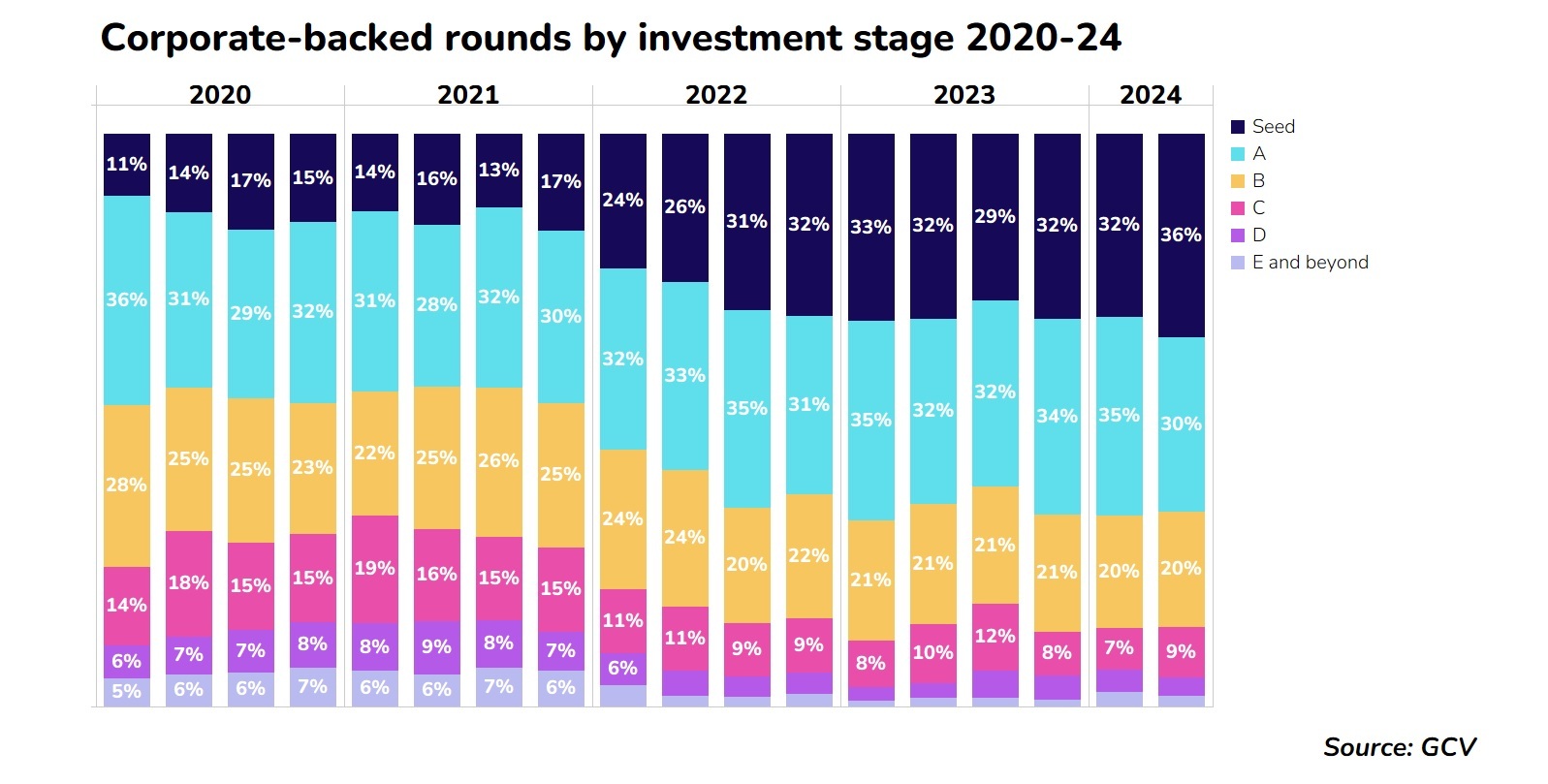

Corporates increase seed investing

GCV data shows that a large portion of corporate investment continues to go into seed-stage funding rounds, a trend we also noted at this time last year. Spend on seed-stage rounds increased to 36% of corporate-backed investment compared with 32% of the previous quarter.

That is more than double the 14% that went to seed-stage rounds in Q2 of 2020. Growth in seed-stage funding began to take off at the beginning of 202, roughly, the start of the post-covid downmarket. From the second half of 2022 onwards, seed rounds have consistently accounted for about a third of all disclosed corporate deals.

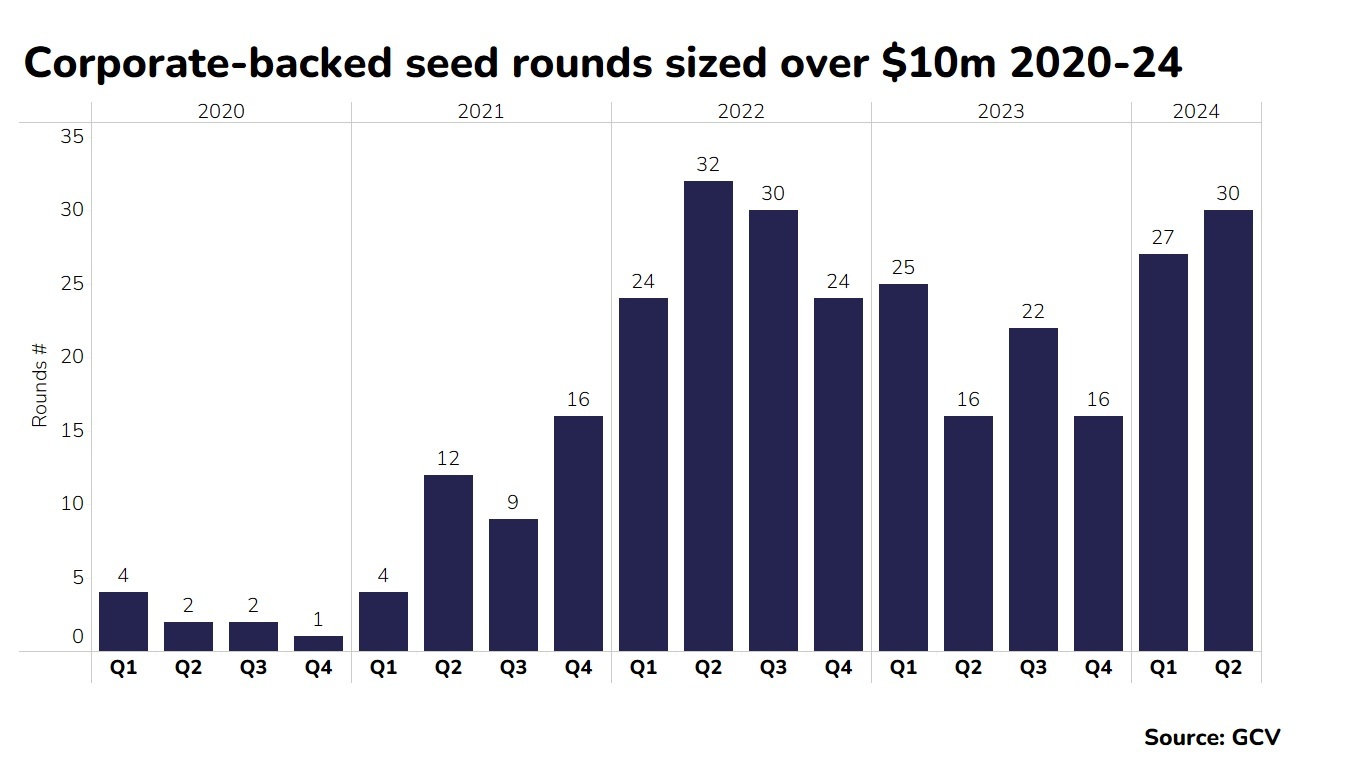

Corporate-backed seed rounds in particular have been growing in size. In 2020 a seed round with a corporate backer would rarely exceeded $10m, but now this is fairly commonplace.

The largest seed round of the quarter was $220m raised by French AI company H Company. H provides artificial intelligence models within the technology sector. Backers included Amazon, Samsung and UiPath as well as several other financial VCs and individuals.

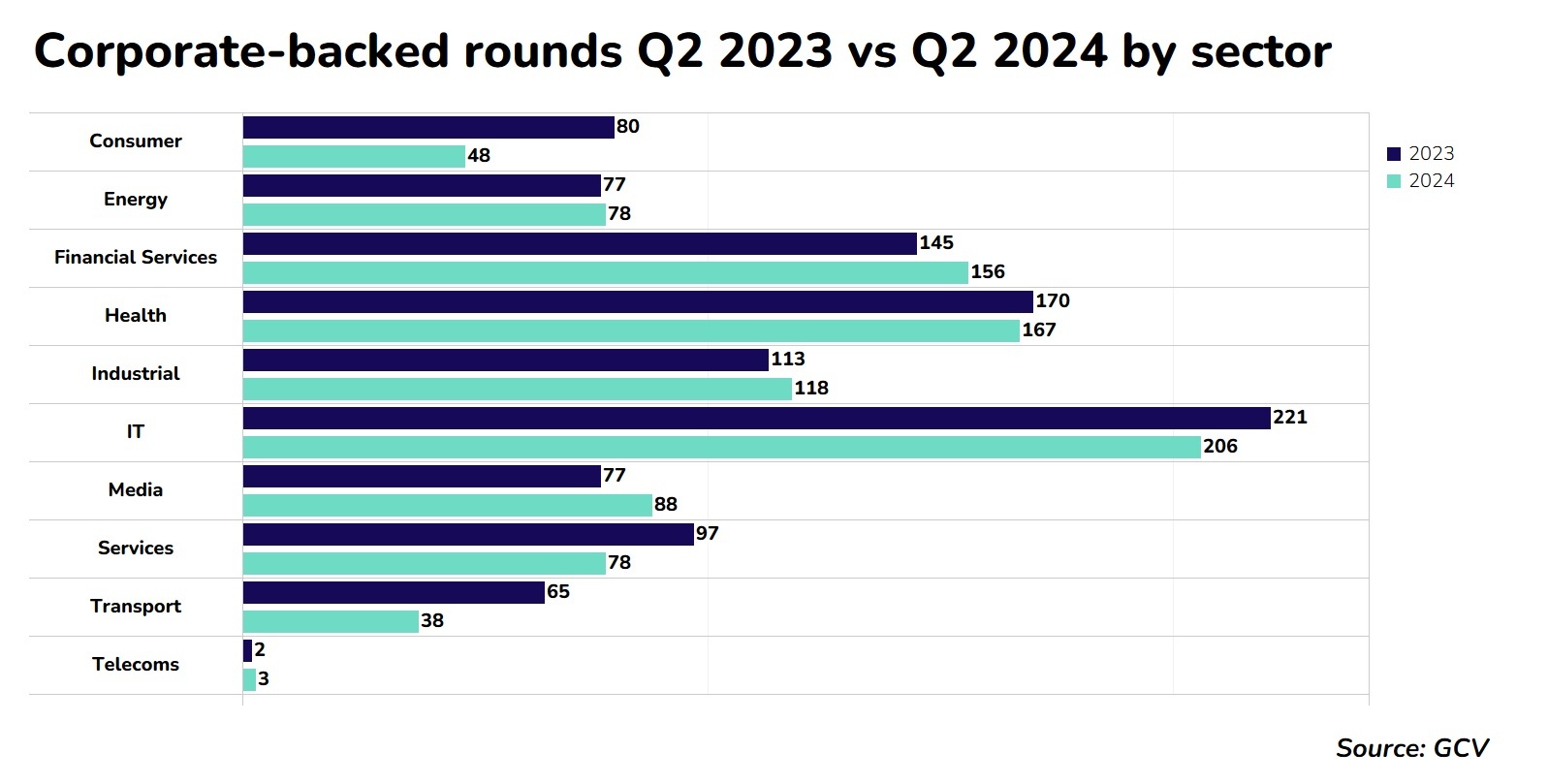

Media sector sees a boost of corporate interest

If we look at corporate backed funding rounds by sector, it’s interesting to see that media companies have seen an increased level of interest from corporate backers. Year-on-year comparisons show that there were 88 media funding rounds with a corporate backer in Q2 2024 compared to 77 in 2023.

In the largest media funding round of the quarter, French TV heavyweight Canal Plus invested $100m in Hong-Kong based telecoms group Viu, taking its stake to nearly 37%. Turkish game developer Spyke also secured $50m from game development company Moon Active. In fact the gaming sector is experiencing an increase in corporate investment, a trend we covered in our April analysis.