AI and quantum, as well as long-term, large-scale energy storage are trends at the top of energy investors' minds for 2024. Exits, less so.

Investors in the energy sector are moderately optimistic about 2024 and expect the investment climate to be generally favourable. The digitisation of the energy industry brings opportunities, although investors are not hopeful about exits.

“In good times and bad times, we aim to keep our investment pace steady and stay the course. So, we will continue to stay the course – that is my anticipation. We invest through cycles,” says Kemal Anbarci, GM of Venture Capital at Chevron Technology Ventures, the venturing arm of oil and gas major Chevron.

More forecasts for 2024

- Transport in 2024: investors eye pick-up in startup deals after a stalled year

- Logistics in 2024: Labour shortages and climate to drive investment

Not all of oil and gas CVCs have necessarily kept the same pace of investments throughout 2023, however. Some have opted to tactically wait: “In 2023, we have really slowed down our investments, waiting for the markets in cleantech to follow the rest of the VC sectors, but suspect it still has some way to go (down). I do believe investment from us might pick up again by H2 of 2024,” says Geert van de Wouw, the head of Shell Ventures.

In the wider energy market, beyond the oil and gas majors, there is a little more optimism: “We do expect to continue investing at our usual pace in 2024,” says Crispin Leick, managing director of EnBW New Ventures, the CVC arm of German utility company EnBW Energie Baden-Württemberg.

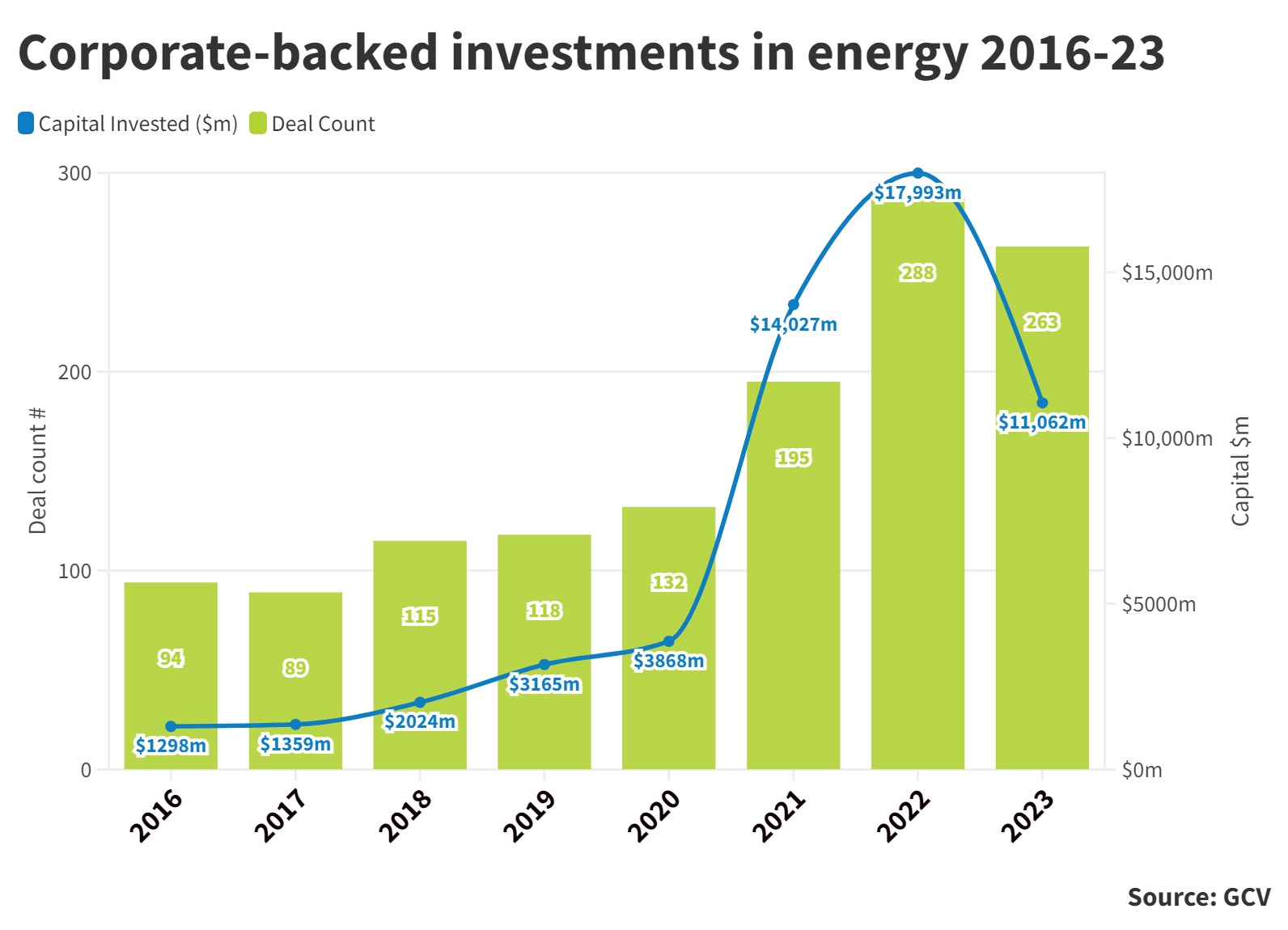

By mid December 2023, we tracked 263 corporate-backed investments rounds raised by energy startups, down 9% from 288 in the previous year. Similarly, the total estimated dollar value of those rounds stood at $11.06bn, down 39% from the estimated nearly $18bn in 2022. That decline, however, is less dramatic than in many other sectors.

Trends to watch in 2024: AI, quantum

Like many other industries, energy sector investors have AI on the top of their mind for 2024.

“I see a trend, looking into next year. AI-enabled services along with edge computing will gain momentum,” says Anbarci of Chevron. “We haven’t seen yet the full impact of what some call “Industry 4.0”. This is likely to unfold and gain momentum thanks to high computational power on the edge. It should enable the further mixing of workers and robots in industrial sites.”

Anbarci also sees enormous potential impact from advances in quantum computing, which could further enable this trend: ”We are on the precipice of a big change with quantum computing. We have seen advances in CPUs and GPUs and I think we are not too far from the moment we will see that QPUs will be integrated with other processing units to deliver step change in computing. This will have great impact on AI and automation. I’m really excited about it.”

Other investors like Leick of EnWB New Ventures see the proliferation of AI-enabled applications as a continuation of the broader digitisation megatrend that has been going on for a while and that is now accelerating.

“Most of our startups are already working with some form of AI and it is technology that you must have and pay attention to build a successful business today. What is new, however, is the speed. We see an enormous acceleration thanks to higher computing power. So, I see it more as a continuum but the speed is now amazing,” he says.

Leick has also identified another big opportunity in ESG data management: “There is a huge ESG data issue for large corporations, as governments are enforcing laws and pushing it. A lot of data management is therefore needed for compliance purposes. This constitutes an enormous opportunity. We have seen the first wave of funding rounds with ESG [data] startups over the past 12 months but we have so far remained on the sidelines. However, we are expecting to deploy capital in the second wave, going forward, as the solutions become more commercially viable.”

Storage opportunities

Aside from digital tech supporting energy applications, there is also excitement about hard energy tech, too, especially storage.

“I expect grid-scale energy storage tech to pick up somehow, as those with close to commercial scale pilots will be an interesting potential investment,” said Anbarci.

For Leick, at utility company EnBW, grid-scale battery storage is also crucial. “Electrification is the name of the game but not just in transportation, it is also at home with the increasing use of photovoltaics and other renewable energy sources, which brings the issue of intermittency to the forefront. This is why large-scale battery tech is getting huge,” he says.

EnBW New Ventures in many of the applications enabling battery technology to become more efficient. One of its most recent investments was in Volytica, which has developed an intelligent cloud-based independent battery analytics platform to analyse the battery condition and simulate the performance behaviour in the future and ensures safety.

Van de Wouw at Shell is also looking into long-term power and heat storage as one of a number of focus areas. But say the team will “double-down on things like renewable energy molecules (H2, biofuels and biogas, power to energy products)”. Decarbonisation technologies such as direct air capture, carbon capture and storage, and nature-based solutions are also on the radar for 2024, as well as digital trading platforms for energy.

Stabilising interest rates

The energy sector already encountered some headwinds in 2023. A number of green hydrogen projects, for example, were delayed in Europe as well as Canada.

“Interest rates rising obviously have had an impact, making it more difficult for large asset rollouts and making projects more expensive,” says Leick. However, he expects the situation to begin to ease this year.

“There are deflationary tendencies now in China and recessionary factors playing out in the West, which will tame any further interest rate rise,” he says.

”With interest rates stabilising, we will see new balances being established and after 2024 things might improve again. The economy and markets were overheated back in 2021, so we are now cooling down to a reasonable level.”

CLA threat for startups

Over the course of last year, there have been some anecdotal concerns, noted by GCV, about the increasing use of convertible loan agreements (CLAs) as way of financing startups during this down market.

The practice involves giving a loan (sometimes called “bridge loan”) to a company that has seen its valuation slashed during the bear market. Investors and creditors make the arrangement in hope that the company’s valuation will recover sufficiently by the time the loan comes due. Under that favourable scenario, the company can raise more equity capital at a much higher valuation and repay its obligations. But this approach can backfire in a prolonged bear market, leading to liquidations of startups that may have taken such loans.

“The increasing use of CLAs could be a big issue for companies that have previously raised capital at excessive valuations,” says Leick. “Luckily, we don’t have any of those in our portfolio. As a matter of fact, we have decreased our outstanding convertibles over the past year.”

This will be an issue to keep an eye on not only in the energy sector but for the entire VC and innovation space.

Exits may pick up by the year-end

Optimism about investment opportunities does not into hope for more exits next year.

“I suspect that 2024 will continue to be a slow year for exits, picking up at the end of the year,” says van de Wouw of Shell Ventures.

“Predicting exits in our sector is like trying to predict the oil price. Most people get it wrong. However, considering valuation corrections we have all seen in later stage deals, it doesn´t seem like the market is ripe for a pickup in exits,” says Anbarci of Chevron Technology Ventures.

But the general outlook is not entirely bleak. “We scored three exits in 2021/22 and another two in 2023,” points out Leick. “So, high quality startups that have not seen crazy valuations can most certainly make it!”