GCV has spoken to several corporate and VC investors about the recent hit to Australia's startup scene following a post-lockdown deal surge.

“We’re seeing term sheets get pulled, we’re seeing valuations get halved, all sorts of things,” says Danny Gilligan, managing partner of Reinventure, the Australia-based venture capital firm funded by local financial services firm Westpac.

It’s a view shared by many other investors in the country.

Activity in the global markets has been down in recent months and the fall in market capitalisation for publicly listed tech companies is now actively impacting round sizes and valuations in Australia even at early stage, multiple figures there told Global Corporate Venturing.

“We’re seeing the same things,” says Anthony Johnston, who formed corporate VC unit Ogilvy Ventures within public relations firm Ogilvy in 2014 and who is now CEO of corporate-to-startup partnership facilitator CoVentured. “If you’re at seed or pre-seed, something that was $3m is now $2m, and that’s a big difference for a business that size.”

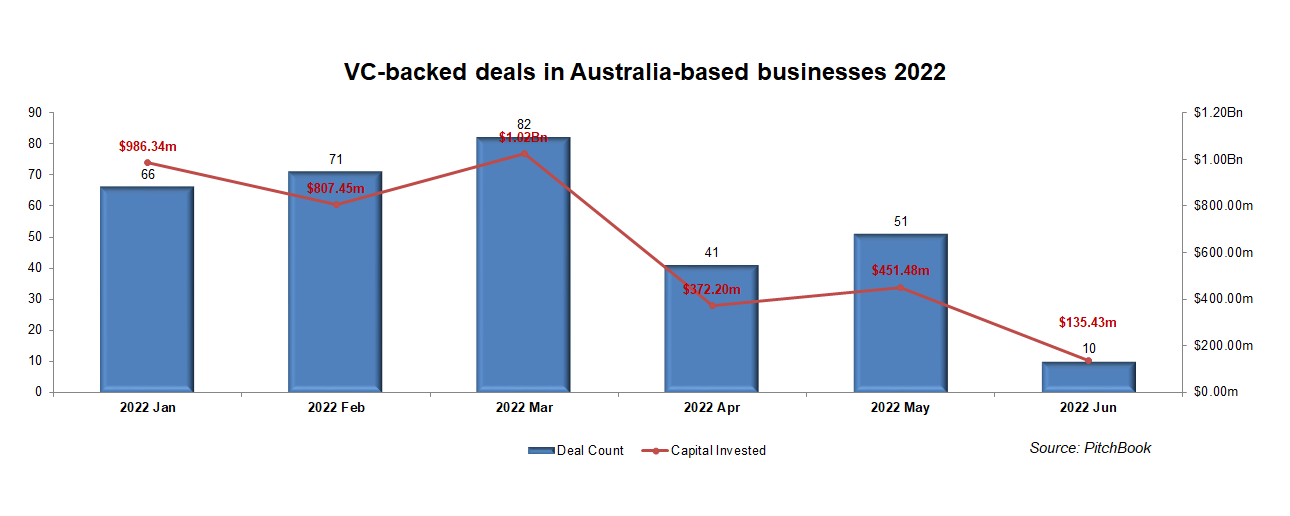

Pitchbook data shows deal numbers have fallen sharply in Australia since the end of Q1 this year, going from a high of 82 in March to just 51 last month, while the volume of cash in those deals more than halved from $1.02bn to $451m.

“There has been a really significant pullback from Australian investors”

Albert Bielinko has been an Australia-based venture investor for Telstra Ventures, the VC firm spun off by domestic telecommunications firm Telstra, since 2015, and is witnessing similar patterns.

“I would say, with the recent drop in valuations along with the market, we have five companies we invested in when they were private and which are now public, and all five have seen really significant valuation drops,” he says. “Their share price has dropped quite significantly.

“There has been a really significant pullback from Australian investors from what I’ve seen in my conversations with our portfolio companies and what they’re observing.”

Johnston adds: “VCs aren’t signing as many deals because valuations have changed, and capital is going to change the way it deals with startups.

“On the CVC side, the corporates are going to be tightening some of the criteria that any type of investment is going to need to be able to benefit the core business and the CVC units if they have a strategic and financial remit.”

Prisoner of Society: Australia’s VC scene during lockdown

The slowdown comes after heightened funding activity over the previous 18 months, as investors supercharged a market that had initially slowed in early to mid-2020. Australia pursued a net-zero strategy for covid-19 that involved shutting its borders, a move which in turn dramatically hit the country’s tourism industry and impacted its economy, initially changing corporates’ priorities.

“On the corporate venturing side, things went really quiet,” Johnston says. “I think the appetite for partnering with startups decreased because the incubator component of trying to help a business along became less appealing when revenue and cost became more prominent.”

“We had 80% of our portfolio get a pandemic kick and 20% got a hard freeze.”

For Reinventure, the caution came directly from its banking financier, a feeling not shared by the firm itself.

“Westpac were telling us it was all doom and gloom, a ‘choose your winners now and forget the rest in your portfolio’ kind of thing,” Gilligan says. “We weren’t seeing that on the ground.”

“What we were seeing was the startups [in our portfolio] that were selling to enterprises had a pipeline freeze because big enterprises were really prioritising how to get their workforce to work from home, how to digitise, how to really become pandemic ready.

“There was no capacity for things that were kind of new and interesting, but for anyone else selling to [small and medium-sized enterprises] or consumers, we just saw this massive acceleration of digitisation. We had 80% of our portfolio get a pandemic kick and 20% got a hard freeze.”

A lot of corporates initially opted to invest quickly off their balance sheets rather than through dedicated units due to the necessity to solve urgent problems before the space as a whole picked up pace, according to Johnston.

“It did go quiet, and then it went really quickly when the capital ecosystem worked out which sectors were going to benefit, and then there was a bit of a scramble. If you had a service-related business, it was tough going.”

The Nosebleed Section: Funding activity hits new heights

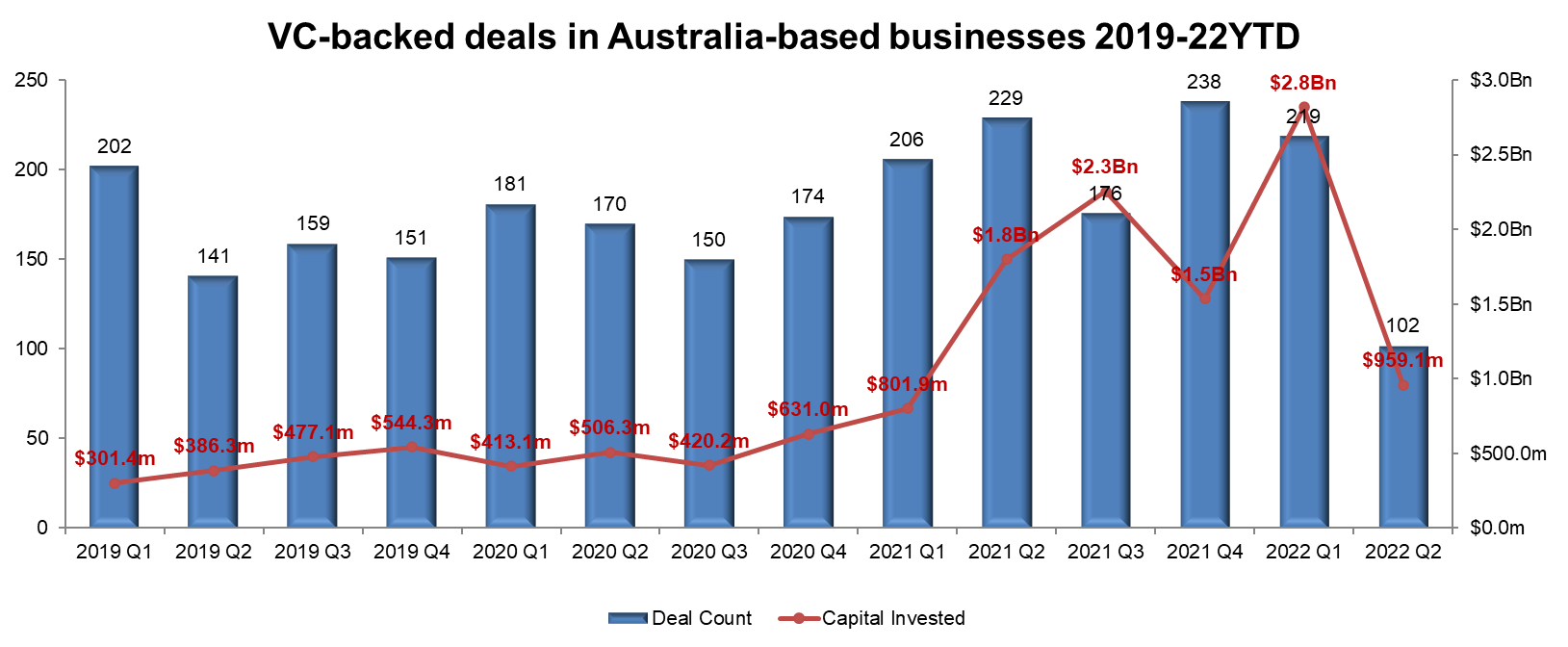

Deal number ramped up to new heights in 2021, peaking at 238 in Q4, while the volume of capital in each individual quarter was comfortably above any in the preceding year and more than doubled from Q1 to Q2.

The Australian startup space was boosted by the large quantity of dry powder available. Telstra Ventures was still investing out of a Fund II that reportedly closed at $500m, but several domestic VCs including AirTree Ventures and Square Peg Capital had closed nine-figure funds pre-pandemic.

When VC firm Blackbird Ventures announced a $356m fund in August 2020, it was a sign the space was pushing full steam ahead. The move to a remote investment process combined with quantitative easing meant US-based funds were also far more eager to invest in places like Australia without needing to see significant annual rates of return or an established business model.

“I think across the board, startups saw almost unnaturally aggressive investors that were keen to deploy,” Bielinko says. “I heard lots of stories of very early-stage startups raising at attractive valuations and really large cheques really early, in some cases millions of dollars offered to startups that hadn’t really proven market fit yet.”

“The laggards have really come on”

The surge in funding also helped precipitate advancement in the domestic corporate venturing space, with the likes of supermarket chain Woolworths making their first investments and others, such as mining group BHP and enterprise software producer Atlassian, establishing formal investment arms.

“The corporate VC scene (in Australia) probably looks much more like other markets now,” Gilligan says, adding that most major companies in the grocery, banking, telecommunications, media and insurance sectors now have some kind of corporate venturing model in place. The space as a whole still suffers from traditional issues with corporate parents however.

“The laggards have really come on, coming into that domain over the last couple of years. There are still as many different approaches to that as there are organisations, and certainly no standardised model for operating corporate venture capital in this market.

“And they still tend to be very focused on things that will help them in the immediate term and not things that could make a difference in the long term.”

Riptide: Where are we going?

Although Australia did not have any particular pandemic ‘stars’ like a Hopin, Getir or Peloton, it is strong in sectors such as cryptocurrency and buy now, pay later (BNPL) services, which experienced exponential growth but which are now suffering in a bear market.

ASX-listed BNPL platform operator Zip Money’s market capitalisation has fallen 90% in under eight months. AfterPay, the BNPL service bought by Block for $29bn earlier this year, revealed that its loss for the second half of 2021 more than quadrupled year on year to $250m as its bad debts more than doubled. But those areas are simply the standouts in a slump which is hitting everyone.

“What we’re seeing more of is the lagging effect of those frothy valuations from last year carrying over to this year and the VC market pulling back,” Gilligan says. “You’re seeing this recalibration take place, coming down from the public markets through later-stage companies and then gradually through to early-stage companies.

“That’s more what it’s about and it’s more an across-the-board resetting of valuations than it is about pandemic-specific companies that are underperforming now.”

Despite those issues and the wider problems in the markets right now, all three see reasons for optimism despite the recognition there are tough times ahead.

“What I see in Australia that is unique is a kind of cockroach mentality for startup founders,” Johnston said. “Founders that are really resilient and able to survive despite whatever is thrown at them.

“One of the ways we’ve witnessed that is through the amount of bootstrapped startups that are able to, without raising a dollar in some cases, actually create sizeable businesses with very little resource.

“I just see less of that in really deep capital markets like the US, and that may simply be because of decades of having the beautiful US capital markets available…the idea of spending less to grow a business is less popular in the US.”

“I don’t see any kind of material change in the ability for good companies to get funded”

Australia’s strong financial technology sector as a factor in its resilience according to Gilligan. Westpac backs Reinventure and the rest of the country’s big four banks – NAB, Commonwealth Bank and ANZ – are all active startup investors to various degrees. He also views its startups as ready to compete in a constrained space.

Reinventure portfolio companies in areas such as SME financing and property technology took a big hit during the pandemic. But they took the opportunity to reengineer their business models and the ones with sufficient cash emerged leaner and stronger with more digitally advanced offerings.

“I’ve not seen any material layoffs in this market,” Gilligan says. “There are a few companies that hit the wall or sold out, but with those there were early indications that was going to be the case early in the pandemic, as opposed to right now because of the change of environment.

“There is lots and lots of dry powder in the Australian VC market, so I don’t see any kind of material change in the ability for good companies to get funded. I think there will be a regression to mean on valuations, and terms which won’t be as founder friendly and will perhaps be a little more investor friendly in this next wave.”

Pandemic or not, a plus point for startups founded in Australia is that scaling in 2022 is easier because the likes of Atlassian, AfterPay and design and publishing software provider Canva have shown you can expand internationally while retaining your domestic headquarters. That pipeline is now established, while local investors understand the process and are willing to get out of the way.

“There is a huge number of unicorns now compared to even two or three years ago,” Johnston says. “That pipeline is healthier and that rubs off on the rest of the ecosystem because there is more knowledge there to provide good mentoring, assuming you can find the right capital.

“Good businesses will find capital but it’s that range of businesses that aren’t great yet but which, with a bit of capital could be great. They’re the ones that are the most vulnerable.”

Photo courtesy of Caleb Russell via Unsplash.