"Resiliency-phase" units move away from CEO supervision, invite business units onto the investment committee and make multiple investments in other venture funds.

Corporate venture funds are surviving longer these days.

The old joke used to be that the average duration of a CVC fund was four years — not enough to go through a full venture investment cycle of seven-to-10 years. But this is no longer true. Most CVC funds — some 60% — surveyed in last year’s GCV Keystone annual survey had been in existence for more than this four-year mark.

There is also a growing group of CVC units that have been in operation for more than 10 years — since 2014. Some 17% of corporate venture teams we surveyed have reached this level.

GCV calls this the “resiliency phase” of CVC, because at this point the unit will likely have survived several corporate changes and market cycles. Well established, their value is well-understood by the corporate parent and they have become less likely to be derailed by events, internal or external.

The big question is — how do you get to the resiliency phase? If you are a relatively new CVC unit, how do you make sure you get into the 10-years-plus club?

We used the data from the 2024 GCV Keystone survey to analyse how resiliency-phase CVC units differed from the overall group of corporate venture teams.

Help us make the 2025 survey even better!

The annual GCV Keystone study is the world’s largest survey of corporate investors, and allows units to benchmark their performance against global norms.

If you take part by filling in your unit’s data we will send you a free, advance copy of the 2025 report.

Some of the differences are ones you would expect. The resiliency-phase CVCs tended to have a fast investment pace, with some 31% making more than 10 investments a year. Only 13% of corporate venture teams in the overall survey made this many investments.

Long-lasting CVC units were also more likely to invest in later-stage, series C and series D funding rounds, probably because they will now be called upon to participate in the later-stage funding rounds of their maturing portfolio companies. They may also have larger funds, if they have gradually increased their capital allocation over the years.

All of this is simply what you would expect from more mature funds. But there were a couple of more surprising differences.

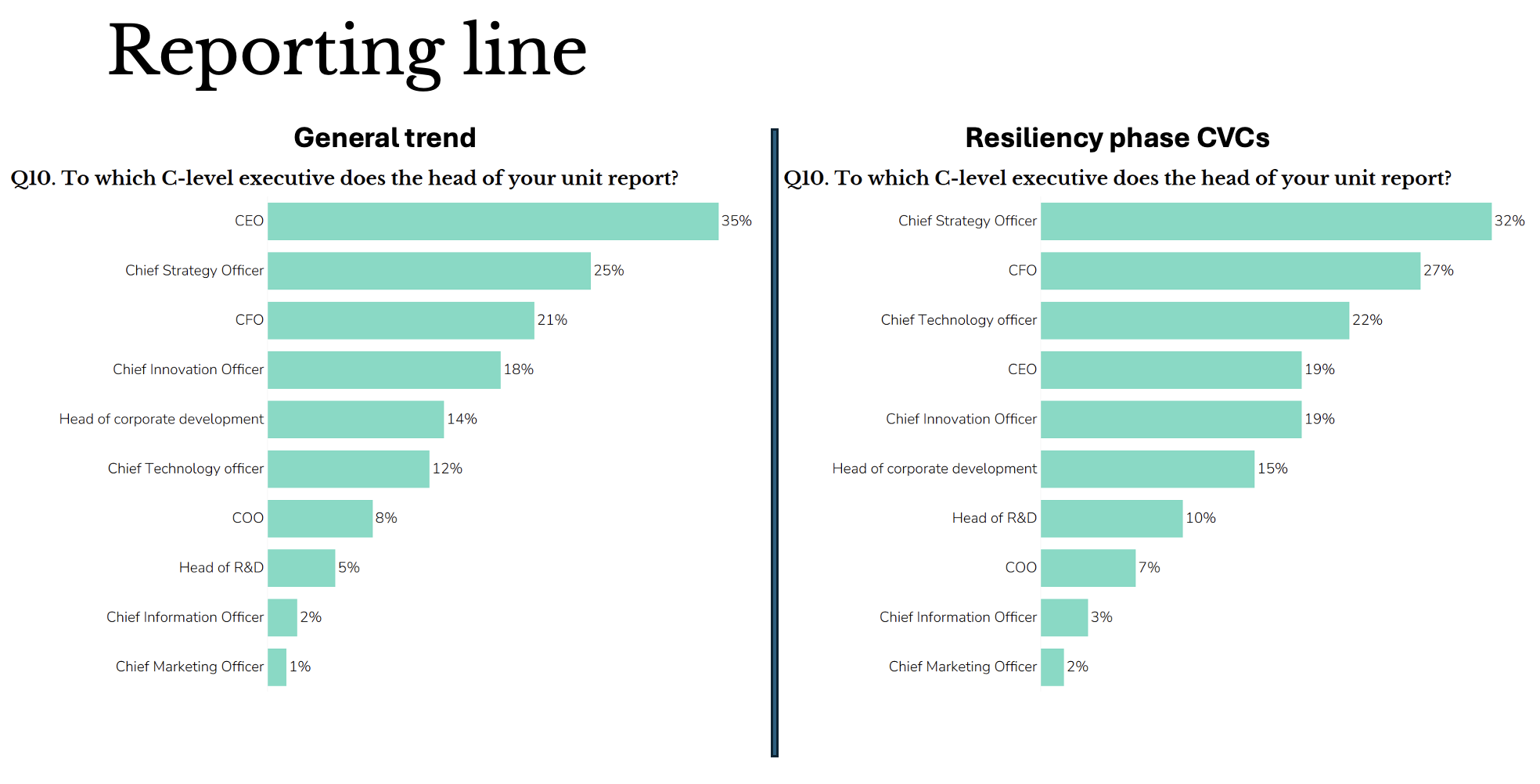

Reporting structure moves away from the CEO

Resiliency-phase CVC units were much less likely to report to the corporate CEO. In the general group, CVC units most commonly — in 35% of cases — reported to the chief executive. But this was true only for 19% of the long-lasting CVC units. It was far more common, in this group, for the unit head to report to the chief strategy officer.

Corporate venturing units frequently shift where they fit in the corporate organisational chart. It is common for one unit to have reported to several different C-suite roles during its existence. But it is nonetheless interesting that for so many of these veteran units, the chief strategy officer is the reporting line they have landed on.

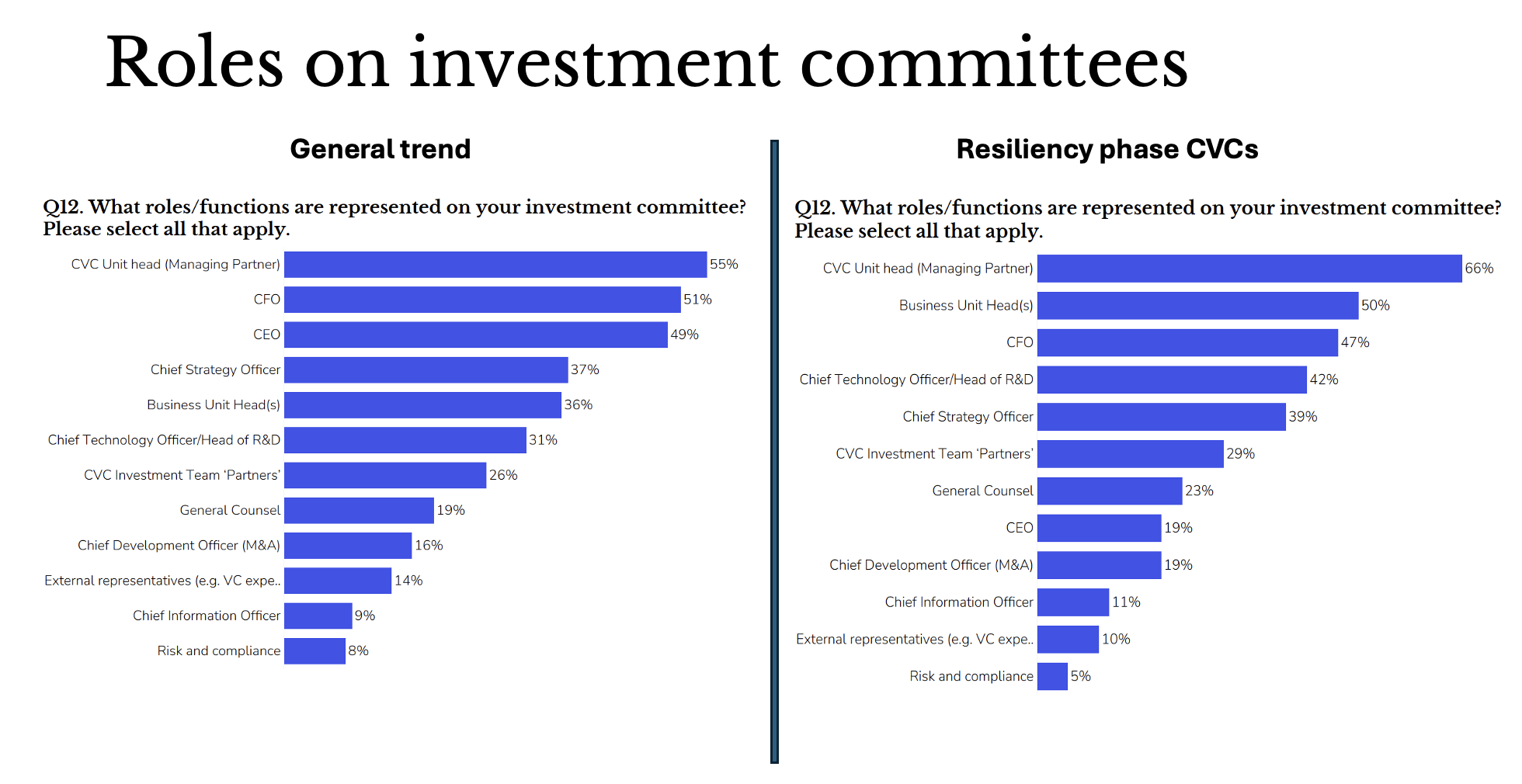

Investment committee embraces business units

The other surprise was the resiliency-phase CVC units were far more likely to have the heads of the corporate business units represented on their investment committee. Half of them had this arrangement compared with just 36% in the overall group.

Involving business units in investment can be a good way of making sure that startups in the portfolio are relevant for real business needs and can go on to have meaningful collaboration with the corporation further down the line.

In the general group it was far more common to include the CEO on the investment committee — 51% did this — while among the long-lived CVC units only 19% included the CEO.

Involvement from the CEO is generally helpful when a unit is being established — support from the top sends a strong message to the rest of the corporation about the value of CVC. But it is interesting to note that, as a unit matures, it is less likely to need a CEO to “babysit” the unit but will instead become embedded across other levels of the company.

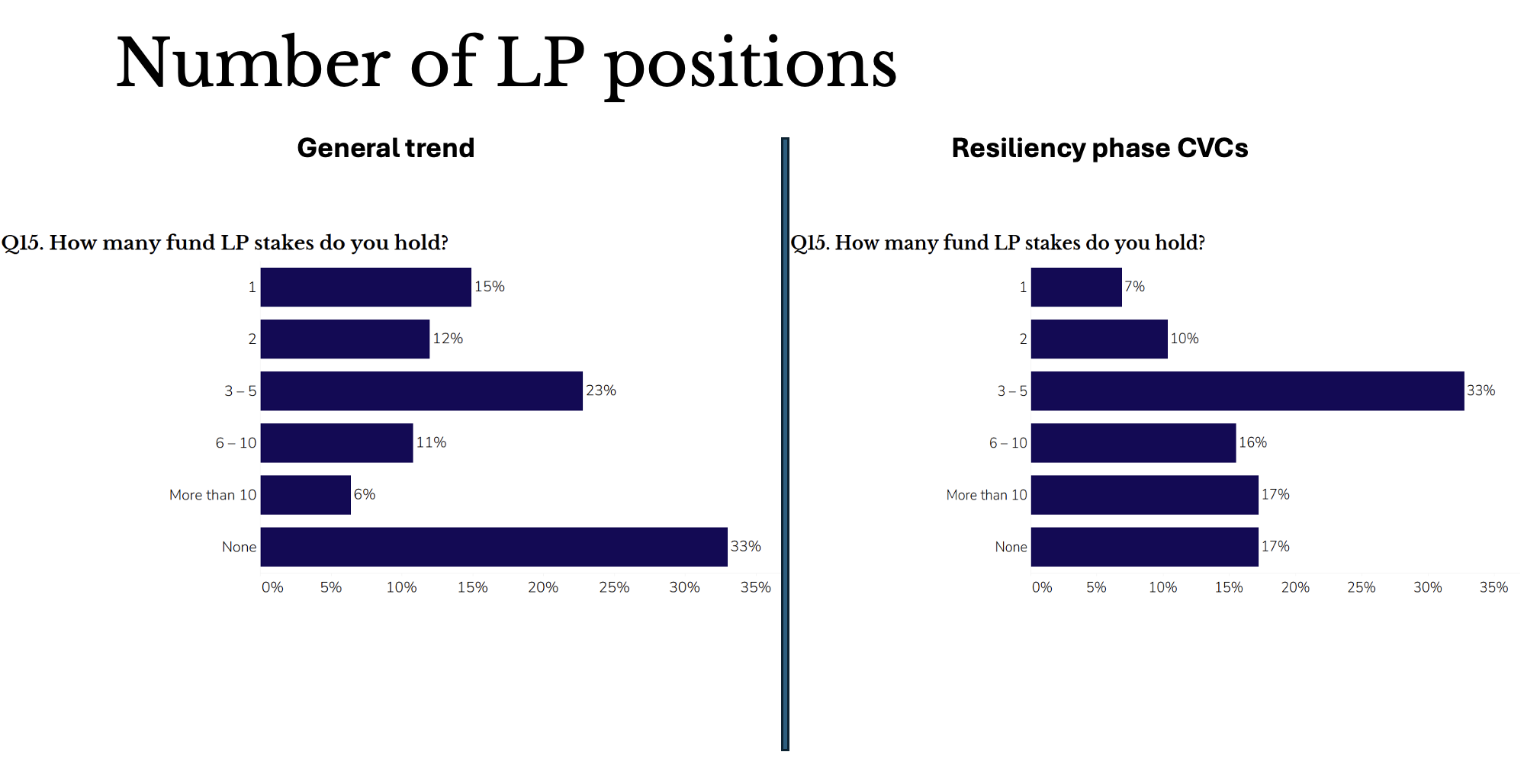

More indirect investments

The final trend we saw was the long-lived corporate venturing units tended to take far more limited partner (LP) positions in other VC funds than the general group. Some 59% of those we surveyed said they invested in other VC funds, compared with 47% for the general group. Veteran CVC units also tended to have a lot of these stakes. Some 66% had stakes in three or more VC funds, while for the general group only 40% were likely to have this many.

This is just a small snippet of the kind of insights GCV Keystone benchmarking survey can provide for corporate venturing professionals. We’d like to make the 2025 survey even better and more comprehensive — with your help and data. Please take a few moments to fill details for your unit. All data is anonymised and all participants will be sent and advance copy of the resulting report. Click here to take the survey.

Maija Palmer

Maija Palmer is editor of Global Venturing and puts together the weekly email newsletter (sign up here for free).