While politicians want to bring tech manufacturing back to western countries, the economics are stacked against it.

With the Biden administration pushing for a decoupling between China and the US, there has been ripple effects across the rest of the world. Europe remains strongly influenced by US politics and is following suit.

Western politicians want to bring tech manufacturing back to its home turf. [See also our recent survey of corporate investors, which suggested that political issues are one of the biggest worries they have about investing in China.]

But while tech companies like Apple are slowly moving manufacturing operations away from China, they’re shifting them over to India, Vietnam and Mexico – not the U.S.

The reality is that bringing manufacturing back to the US or Europe is not as straightforward as it seems, because of the deeply embedded chains built over decades of east-west collaboration.

We believe that western re-shoring will be a long struggle, and that in the meantime Chinese hardware businesses will continue to make excellent investment targets.

1. Rebuilding industrial value chains will take time

The US offshored a significant amount of production, such as electronics, in the 70s, which extended into IT and communications in the 90s. Restoring these abilities requires significant amount of time, investment and effort. Even the most basic of necessities – the humble N95 face mask – required navigating a complex maze of obstacles to have it manufactured back in the US. The irony was US companies had to import materials and production equipment from China to make it possible to manufacture the masks locally. Building a resilient supply chain is expensive as well, just to ensure there are alternative sources and resources. And knowing the bureaucracies of US politics, there’s the challenge of getting all regulatory agencies to work together.

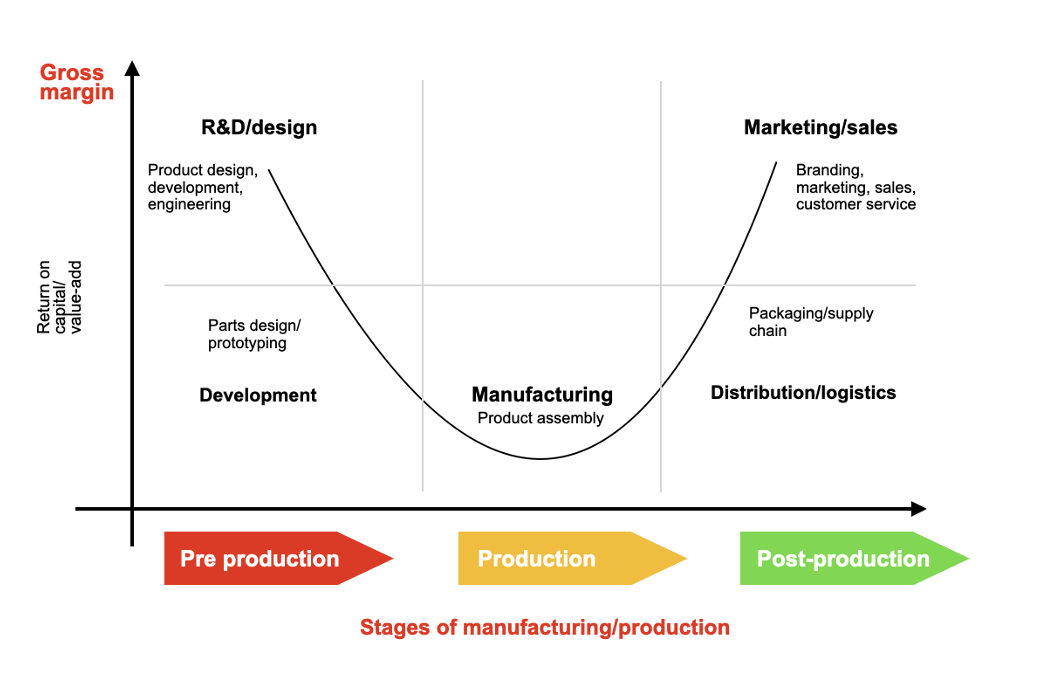

2. Capital markets aren’t supporting manufacturing

Also known as the ‘Manufacturing Gap’ (see smile curve above), where the return on capital is too low for capital markets to invest in, the smile curve hypothesis shows that the manufacturing stage is the least valuable in the entire industrial value chain.

This is very much true: chip designers enjoy gross margins as high as 60%, while companies that produce/assemble the chips average just 17%, according to Bloomberg Intelligence. Currently chip design is dominated by the US market at 68% of market share. But the US possesses just 3% of the outsourced semiconductor assembly/testing market.

“Companies struggle to find banks to finance new factories, especially if it takes up to two decades to pay off.”

In the west, labor is expensive, energy is costly, and companies struggle to find banks to finance their new factories, especially if it takes up to two decades to pay off.

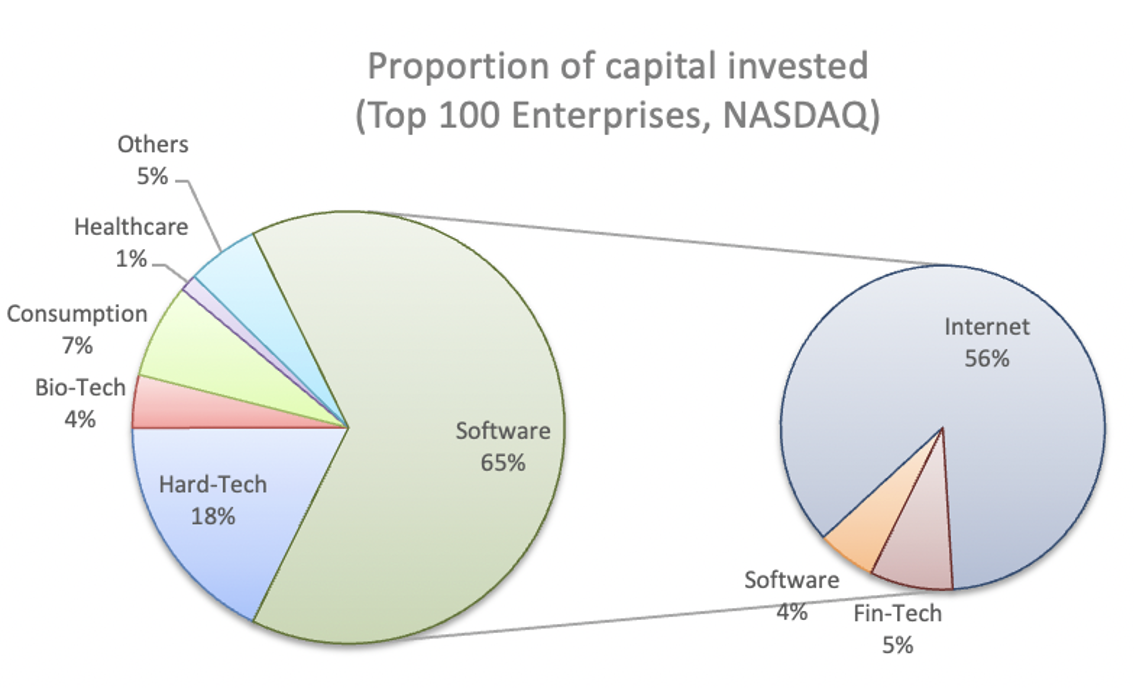

If we look a look at NASDAQ to see where capital flows to – less than a quarter goes to hard-tech. Assuming most of it is R&D, design and marketing, we can expect even less going into the actual manufacturing of the product. However, more than half of all the market capital is invested in software, and the rest are laid across a broad variety of services and fundamentals.

3. The Chips Act and the Inflation Reduction Act will not benefit smaller startups

The Chips Act and the Inflation Reduction Act were passed to encourage bring manufacturing back in the US, create more jobs and protect intellectual property. Subsidies and tax cuts are in place, but we see these mostly benefiting the large conglomerates such as Intel or Texas Instruments. From a WACC (weighted average cost of capital) standpoint, expected returns range from just 10%-15%. For smaller startups backed by VC capital, that only makes sense at 30% internal rate of return. Yet small companies make up the bulk of the market.

And as S&P Global Market Intelligence reports, “there are also plenty of challenges that the Chips Act can’t directly address — a complex brew of economic factors, logistical bottlenecks and disruptions, trade wars, shifting geopolitics and (not least) technical barriers — that could mitigate any positive impacts attributable to the Act.”

4. Did we not learn from the clean tech bust a decade ago?

The 2011 Solyndra bankruptcy was a valuble lesson for many tech investors, a spectacular failure in the clean tech bust at the beginning of the 2010’s. In total, government grants worth $1B went up in smoke — it was quite exceptional that a single clean tech company was able to receive so much in grants. The concept of solar energy drawn from a revolving tube of alternative solar-sensitive materials was interesting, but the delivery and execution left much to be desired. This can be attributed to 3 primary reasons:

a) Extremely high cost

From R&D to manufacturing to distribution, several teething issues weren’t resolved. Solyndra invested in a very expensive custom machine that couldn’t reach its expected output. In the end, a Solyndra module’s production cost 30% more than a traditional solar panel.

b) Slow ramp-up

The timing was poor. In 2008, polysilicon prices, a key element for solar panel production, was $300/kg. By the time the federal government approved Solyndra’s loan, the prices fell to $50/kg. Natural gas prices fell as well, contributing to lower energy prices. At the same time, a flood of Chinese-made solar panels became a much more viable option.

c) Slow to revenue

Private venture capital funds typically work on 3–5-year horizons. Energy and environmental technology initial offerings on traditional exchanges take an average of 8.3 years.

As TechCrunch reports, “Solyndra had the innovations, but it didn’t get to the price point where it could compete, not only with other energy sources, but even with the conventional solar panels it was trying to disrupt.”2 The combination of factors – the 2008 financial crisis, cheaper natural gas, China’s affordable quality solar panels – formed the perfect storm to fell Solyndra.

We’re starting to see the same thing happening today. Remember Nikola, touted as the global leader in zero-emissions transportation, energy supply and infrastructure solutions? The stock (NKLA) price is down 70% today. And chip plants aren’t cheap. Or easy. Building a chip plant in the US is several times of what it costs in Taiwan/Asia. Just an entry-level plant in the US will cost $10-$20 BN, and up to 5 years to build. Let’s not forget operational costs. A chip plant requires an average of 4.7 million gallons of water a day – unable to meet today’s ESG requirements. A semiconductor engineer’s salary in the US is $118,300/yr, while the same engineer in Taiwan is paid $32,500/yr. If we do the math, many of these costs will be passed on to our pockets: the consumers.

“One of the big reasons for this is that the cost of labor is lower, and it’s just far cheaper to produce at a very massive scale, integrated circuits and chips, in those parts of the world (Asia),” says Columbia Business School professor Dan Wang. Morris Chang, the founder of TSMC, said that it costs 50% more to manufacture chips in the U.S. than in Taiwan.

5. Sure, but what about Tesla?

Of course, many will cite Tesla as the most obvious, the most successful, hard tech company out of the US. It is worth noting that aside from the US, Tesla has built factories globally in markets where they are popular: Germany to China. Two very important points stand behind its success:

(a) Tesla is a direct-to-consumer company. There are no middlemen costs in between. Even more so with their factories located in customer countries.

(b) The founder, wealthy from his recent sale of Paypal to Ebay, assumed Tesla’s earliest startup risks heavily with his personal funds.

We can safely assume that 99% of all startups in materials or hard tech don’t have, or can, afford that model.

Fact: a single man-portable Javelin surface-to-air missile used to defend Ukraine against Russia contains over 200 chips. But life-saving medical technology, such as systems that help develop vaccines, require chips as well (just far fewer chips per device). For industries beyond the military scope – which is most of the market – tech manufacturing driven by primary economics wins hands-down.

When bringing tech manufacturing back to shore is motivated by politics, it inevitably increases costs for everyone, due to the lack of consideration for economic fundamentals. Even with a substantial investment of capital and resources, a clear and present risk of failure remains. While there is a resurgence of hard-tech startups in the market, we prefer to remain cautious – as we, like all capital investors – must look at the hard economics first.

We believe in this because our investing philosophy centres around not just the science behind the tech, but also the macro/micro-economics that give it reason for being. It is one of the reasons our investments regularly deliver positive results.

“We can expect this to be a long value chain struggle.”

In conclusion, we can expect this to be a long value chain struggle. While there are plans and steps in place to close that manufacturing gap in the west, it will be years, possibly decades, before that becomes a common reality. Until western manufacturing costs fall to a level that can beat Chinese manufacturing outputs, the advantage of Chinese manufacturing cost, quality and experience remains our preferred reality for now.

Dr. Min Zhou is the CEO of CM Venture Capital, a China-headquartered investment company which partners with a number of multinationals to help them invest in cutting-edge hardtech.