There were 42 corporate-backed startup funding rounds in China in February, up 27% from the previous month. Most of these were backed by Chinese tech giants such as Tencent and Baidu.

Chinese corporations increased their investment in domestic semiconductor and AI startups sharply in February, a sign that China is ramping up its domestic capabilities amid an escalating trade war with the US.

There were 42 corporate-backed funding rounds in the country in February, up by 27% from January, and 11 of these were in the IT sector. Investment in these startups is coming from Chinese tech leaders such as Tencent, Baidu, Ant Group and Lenovo, although Korea’s Samsung is also taking some bets on Chinese IT startups.

Headline trends from GCV’s CVC Funding Round Data for February showed that:

- Deals were up 21% in volume but down by $2bn in value. The dollar value fall is arguably less severe than at first glance, however, due to skews in the 2024 data. The average deal value of <$1bn rounds fell by $1.1m.

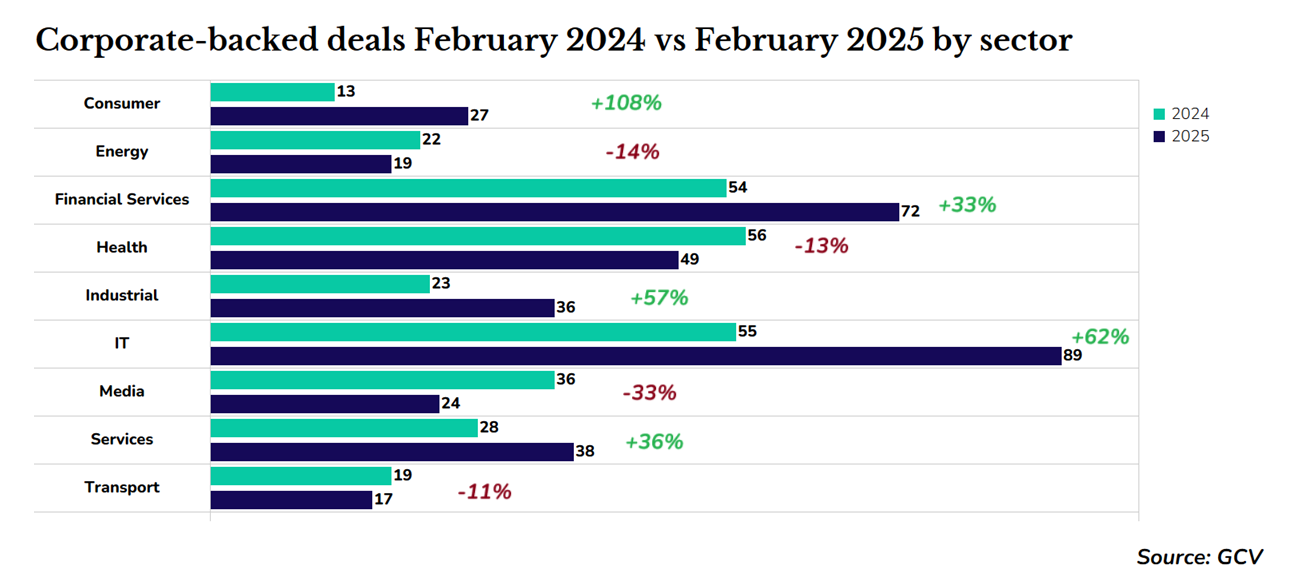

- The finance and IT sectors saw the largest absolute increase in dealmaking volume year-on-year. Media saw the sharpest fall.

- There were no funding rounds totalling over $1bn. Some 23 rounds exceeded $100m, compared to 28 in February 2024.

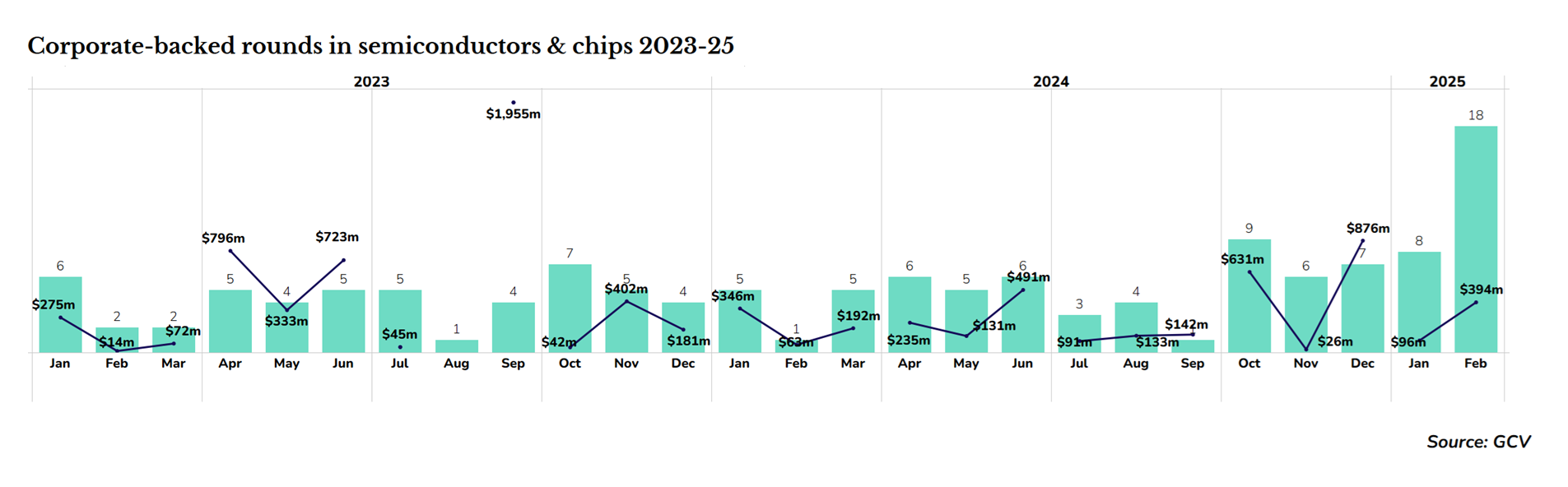

- Semiconductor startup investments reached a two-year high, driven largely by Chinese activity, which accounted for eight of the 18 total deals.

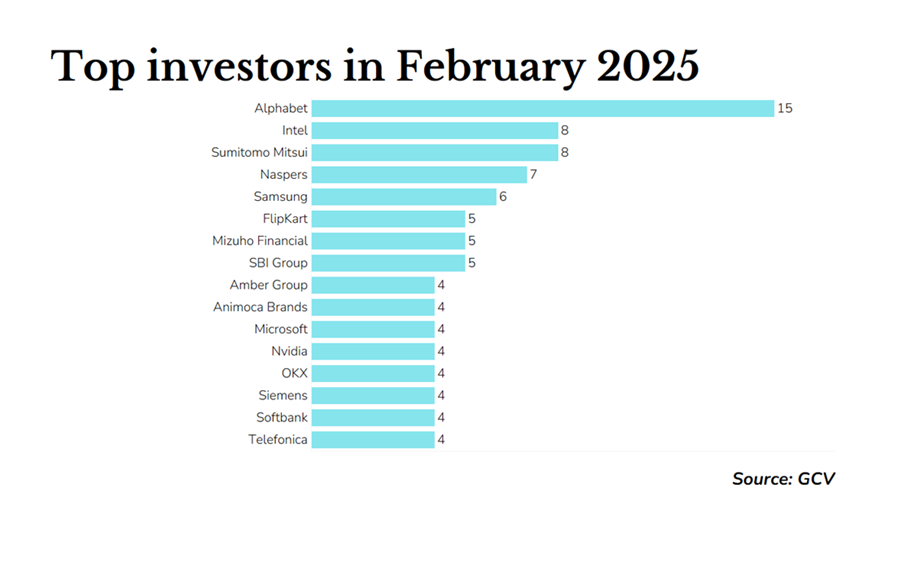

- Intel Capital leapt up in dealmaking volume in the month to reach joint-second place for the most active investors, closing eight deals. It was announced in January that the CVC unit was spinning out from the parent company.

February 2025 data overview

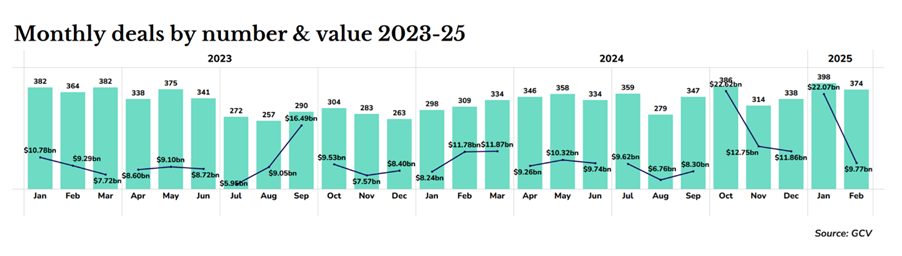

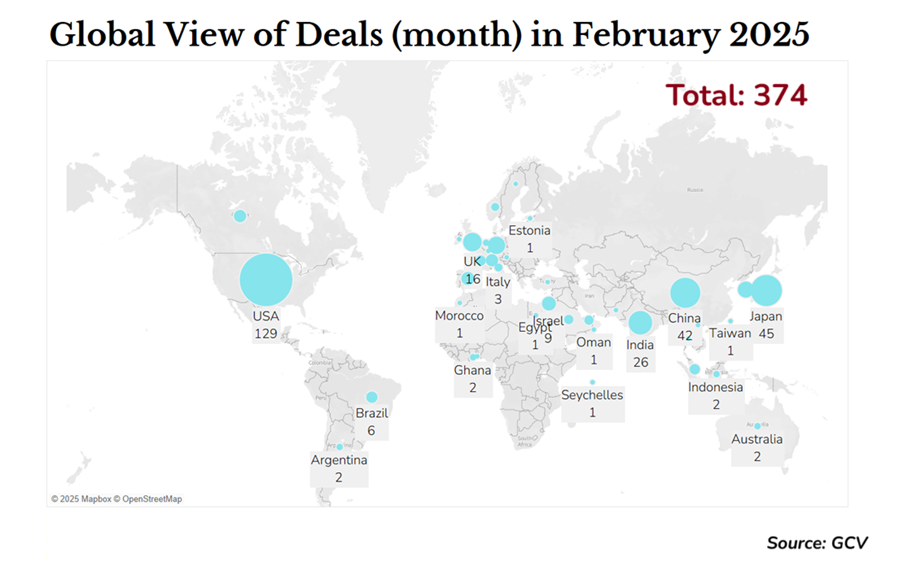

There were 374 corporate-backed funding rounds in February. This is one of the highest monthly totals seen in the last 12 months, and is a 21% increase from February 2024.

The main drivers of this are healthy increases in the financial and IT sectors, which are up by 18 and 34 deals, respectively. And while a year-on-year comparison can only tell us so much, when compared against recent months, both sectors still show noticeably strong February figures.

Finance: crypto creeps closer to the mainstream and insurtech sees a resurgence

The increase in finance startups was concentrated in the payment technology and cryptocurrency subsector, where 33 deals were made, compared to 24 in February 2024. One of the largest of these was the $70m funding round for Bitwise Asset Management, a crypto index fund manager.

MassMutual, the US insurance giant, participated in the Bitwise round. This is an example of how traditional finance institutions are taking crypto assets seriously as they grow towards becoming more mainstream, with large asset managers like BlackRock launching crypto exchange-traded funds and stablecoins – cryptocurrencies pegged to conventional assets like the dollar – becoming more popular.

There was also an increase in insurtech deals, which rose 150% from four in February 2024 to 10 this year. GCV has recently reported on how insurtech had had a slow year in 2024 as the insurance industry, beset by rising losses, pared back on investment.

This is an area we will continue to monitor closely. February’s data could be an early sign of things warming up, although it is still too soon to draw firm conclusions.

The German reinsurance multinational Munich Re participated in the two largest funding rounds of the month for insurtech startups, through its CVC unit Munich Re Ventures. These were in the US startup High Definition Vehicle Insurance, which provides coverage for commercial trucking fleets, and Brazil’s Azos, a digital life insurance provider.

In the Middle East, the Qatar Insurance Group announced three strategic investments in one day, as part of its ambition to expand throughout the MENA region and beyond into global markets. These were the US-based MIC Global, Saudi Arabia’s Digital Petroleum and Singapore’s Jaguar Transit.

Semiconductors: China spreads its bets

Of the IT subsectors, the big story for February 2025 was the growth in semiconductor deals.

Some 18 chip technology startups held corporate-backed funding rounds. This is more than at any time in the last two years. GCV’s data over that period has never recorded more than nine in a month.

China made up the bulk of the total, with eight deals, encouraging its domestic innovation as the availability of US technology is increasingly restricted. One of these deals is a designer of chips for use in high performance computing and AI applications, Silang Technology (Smart Logic).

The other startups span a range of applications, including navigation, video transmission and image processing. Puzhao Materials, which makes photomasks, plates used to print integrated circuits onto silicon, had the highest disclosed funding round total for any semiconductor startup worldwide in February, with a $102m series B raise.

In the UK, Scotland-based Clas-SiC Wafer Fab received a $15.2m investment from Indian chemicals company Archean Chemical Industries. Clas-SiC Wafer Fab makes silicon carbide semiconductors, which are more suited for use in electric vehicles and renewable energy systems.

February rounds in dollar value: no (very) big deal

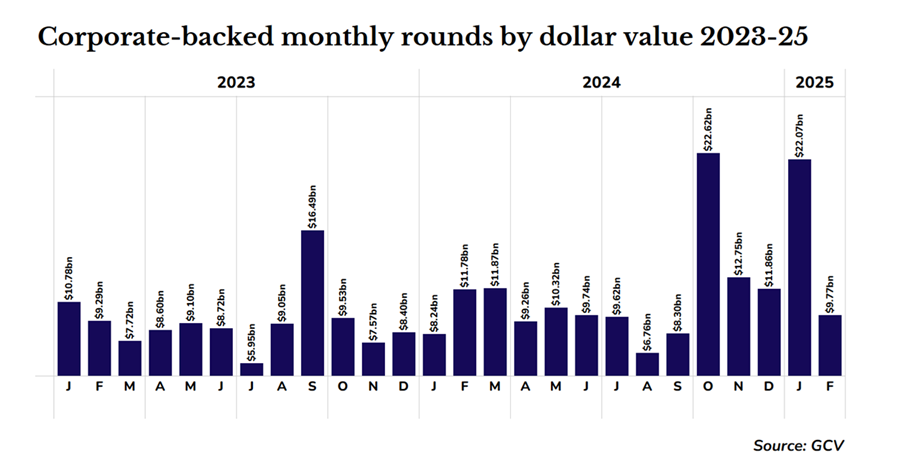

Despite the growth in deal volume, the total dollar value of deals compared to February 2024 was less impressive. For the funding rounds where deal size was disclosed, the total across the month fell by $2bn from February 2024, to $9.8bn, the lowest it has been since September.

But this doesn’t necessarily mean that the growth in deal volume is not translating to more capital for startups. February 2024 saw two exceptionally large deals worth $2.5bn combined. These were into the US video game company Epic Games ($1.5bn) and the Alibaba-led round for Chinese LLM developer Moonshot AI ($1bn). When these two are stripped out of the February 2024 data, the average deal size has fallen, but the drop, at $1.1m, is relatively modest.

Unlike some recent months, including January, there were no funding rounds over $1bn in February 2025.

The largest was the $881m raise from XCMG Auto, a Chinese electric and hydrogen-powered commercial vehicle manufacturer. Its portfolio of vehicles are made for the logistics, construction and mining industries.

Its corporate investors reflect this spread of applications. Among its backers are three large state-owned Chinese companies: the Aluminium Corporation of China, China Logistics Group, and China Baowu Steel Group.

China closes the gap with Japan

Deals data from China can be hard to source, but GCV’s collection method has been consistent throughout the December to February period, giving us reliably comparable data for the last three months. And with 42 corporate-backed funding rounds, China’s deal count is considerably higher than in January and December, where the totals were 33 and 30, respectively. It was only three fewer deals than Japan, which has a highly developed corporate venturing ecosystem and consistently ranks second in the world – behind the US – for deal volume.

More than a quarter of the Chinese rounds were for startups in the IT sector, contributing to the IT and semiconductor surge described above.

It also had the highest amount of corporate-backed funding rounds in the industrial sector, with nine in total. The largest of these was for the advanced materials company Yangzhou Nanopore, which received $137m. It makes materials for lithium ion battery enhancement. Tsao Pao Chee, an industrial conglomerate with business interests including shipping, took part in the round.

Robotics: are we human?

Another trend China’s investment has contributed towards is in the growth of the industrial subsector of robotics, which saw one of the biggest leaps in subsector activity between February 2024 and February 2025. There were 11 deals in the month, compared with two last year. China made four of these in February 2025, compared with one in 2024.

If the scope is widened to include AI companies that make programmes designed for use in robotics, then even more interest is noticeable. Three Chinese startups making AI systems designed for use in robotics received corporate investment in the month. The e-commerce giant Alibaba led a round of an undisclosed size into Corenetic, and Galaxea AI received investment from Baidu, a Chinese AI company.

Of the startups making robot hardware, two of the three largest corporate-backed deals were for companies making humanoid robots. These are the US startup Apptronik, which raised $350m in a series A round which saw participation from Alphabet, and Lingbao Casbot, which raised $13.7m in an undisclosed round, with backing from Lenovo.

Top investors: the return of Intel

Intel Capital, a CVC unit set up by the US chipmaker Intel, invested in eight startups in February. This is a considerable uptick in activity: in both January and December, it made only two investments. In November it made one. This burst of life comes after the January announcement that the unit was to be spun off from the struggling parent company. Intel had also shut down its Israel-based startup accelerator Intel Ignite in September last year. Both moves are thought to be cost-cutting initiatives.

Of the eight February investments, only one was in a startup making semiconductor technology. This was the Spanish company Wooptix, which works on a product for enhancing the manufacturing process. It also received backing from Samsung Venture Investment.

Flipkart is the largest e-commerce company in India, a country that excels in the sector. It announced five startup investments in one day in February as part of its Flipkart Leap Ahead accelerator programme, which is funded by the CVC unit Flipkart Ventures, and targets seed stage companies.

Four of the startups are based in India, including Expertia, which makes an AI-powered HR system to assist in hiring, and Visa2Fly, an online Indian visa application platform. It also invested in the US startup Factors, which makes AI-based business analytics software. None of the ticket sizes were disclosed.