Seed-stage funding rounds have become bigger and more competitive, and many smaller funds are now shifting towards even riskier pre-seed investing.

Multi-billion-dollar fundraising rounds for AI startups have captured headlines in 2025. But what has received less attention is the transformative impact these mega rounds are having lower down the venture capital funding landscape, making funding rounds at all levels bigger and pushing many investors to invest in much earlier-stage rounds.

Seed investing – providing funding for startups that might not even have revenues or a product yet – has seen a dramatic expansion as more mid-range investment funds have entered this part of the VC market. This is partly driven by the fact that it is increasingly difficult for small to mid-sized funds to compete with the mega funds in later stage funding rounds for more mature technologies. Larger funds are also increasingly taking part in early-stage startup fundraisings.

The result is that seed rounds are larger than they used to be and more competitive, forcing corporate investors that had carved out a niche in seed investing to hone their investment strategy so that they stand out more to founders. Some are investing even earlier, looking at pre-seed rounds where valuations are less frothy.

“We’re seeing a definite bifurcation of VC where you have the huge mega funds that are raising billions, and then you have the VCs that are very niche and focused,” says Mike Smeed, managing director of InMotion Ventures, the CVC of carmaker Jaguar Land Rover.

“Then there is the mighty middle, which is getting more and more squeezed as time goes on, because they are neither one nor the other and are in a bit of a danger zone. Some of those mid-range funds are starting to play more at the seed level and series A,” says Smeed, whose investment team targets seed investments.

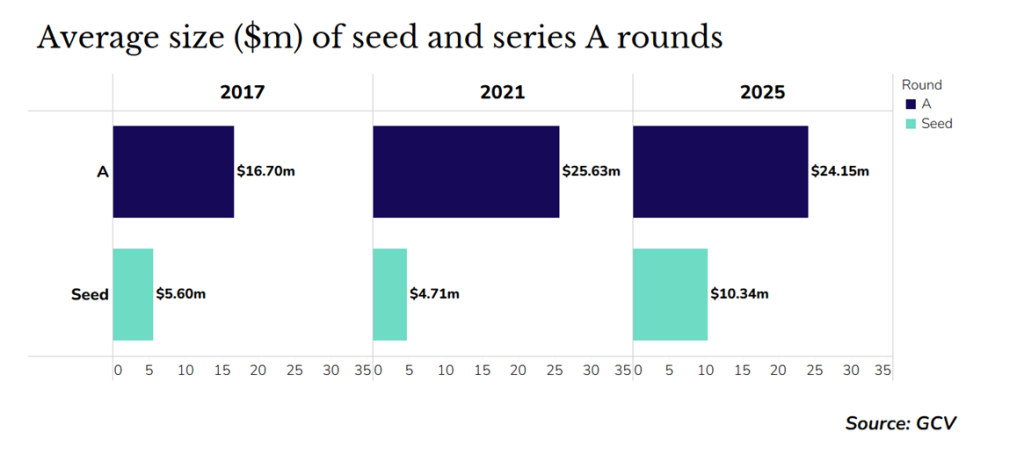

The average size of corporate-backed seed rounds in 2025 is $10.34m, a 120% increase on the average size of deals in 2021, according to GCV data.

Large seed-stage funding rounds that included a corporate backer in 2025 include the $2bn seed capital raise for Thinking Machines Lab, an AI startup cofounded by OpenAI’s former chief technology officer, Mira Murati. Corporate backers in the July fundraising included chipmakers Nvidia and AMD.

Nvidia was also behind the $300m seed funding for Periodic Labs, a startup developing AI research systems for the discovery of new materials and drugs. Large VCs such as Andreessen Horowitz and Lightspeed were part of the September round.

Only about 5% of seed investments raise more than $20m, but the vast majority of these — some 70% — include a mega fund as lead or co-lead, according to research by investment firm Sapphire Partners. On the flip side most seed-stage deals still raise less than $10m, and 60% of these are led by dedicated seed funds.

Some of the dynamics between startups and corporate investors have changed, too. Seed stage startups often welcomed corporates onto their cap table early because they felt the company name acted as an endorsement and a positive signal for other investors. But now, AI superstars like Mira Murati are able to raise large amounts of capital simply because of their name and expertise. This can leave smaller corporate VCs sidelined.

“We always used to talk about the beauty of corporate venture capital was providing the endorsement to a startup and the solution that they were looking to provide. That was the go-to market,” says Smeed. “Whereas now that doesn’t seem to really matter. There are some people who are kind of generational talents who are looking to secure money.”

Startups stuck at seed for longer

With the infiltration of mega funds at later stage and even at seed, startups are also staying longer in the early-stage funding stage as the revenue expectations for series A companies have increased.

Startups with $1m in annual recurring revenues used to be able to raise a series A round, but now investors are often looking for more than $3m. Large investment funds seek to exit startup investments at much higher valuations than smaller ones and so will only fund startups at series A where higher revenue thresholds have been met.

The knock-on effect is that investors are participating in many more seed extension rounds, also known as bridge rounds, which are increasingly required for startups to reach certain milestones.

“There is an elongated period between seed and series A now,” says Elizabeth McClusky, managing director of TruStage Ventures Discovery Fund. “For some of our existing portfolio companies where we thought they would have graduated to a series A, haven’t quite gotten there. So, we are doing follow-ons in a kind of interim round between a seed and a series A.”

The move into pre-seed investing

TruStage Ventures, the investment arm of US insurer TruStage Financial Group, has increased its focus on pre-seed investing where valuations are less frothy than at seed. The investments at pre-seed are riskier given that the technologies are even less mature, but it is worth the trade-off for some CVCs.

“You can get higher ownership percentages and that risk reward trade-off feels approachable at the pre-seed level,” says McCluskey. “At pre-seed it is risky – there is still a lot that the company has to validate – but at least the valuation reflects that.”

The decision to invest in a pre-seed startup is based more on the skills of the founder, a different proposition to seed and series A investing. McCluskey’s team seeks to meet startup founders before they even raise pre-seed rounds. It also seeks to co-invest with investors that can add validation to the technology.

These are the pre-seed startups that were backed by corporate investors in 2025

For a full database of CVC investments at all stages going back to the start of 2023, see the GCV's CVC Funding Round Database

Pre-seed companies would historically have still been in the idea phase. But now, as interest in early backing grows, investors like TruStage Ventures might even look for pre-seed startups to show some revenue. “We are going to be able to have a bit more validation at the pre-seed level than we normally would,” says McCluskey. “Companies raising a pre-seed now may have revenue, they’re in market. You can get into a pre-seed deal that has some traction.”

With more competition in seed rounds, CVCs are having to increasingly show how they stand out as a beneficial investor. Smeed has noticed that startups have much more leverage to demand financing terms than they didn't used to have. In InMotion’s case, startups have started asking for things like guarantees that will commit the corporate investor to doing proof-of-concept projects.