Web3 looks set to be responsible for a flurry of exits as buyers take advantage of friendlier regulation and entertainment companies join fintech as key players.

The Web3 sector – the collective name for all blockchain-related technology – has been one of the busiest for startups in recent years but there has always been one big question mark: exits.

Although cryptocurrency exchanges, NFT marketplaces and digital asset companies have racked up big valuations, regulatory hurdles have meant almost none have gone public, and so far there hasn’t been enough acquisition activity to make up the balance.

But M&A activity is rising for Web3 startups and looks set to continue this year, as a more attractive regulatory system pulls in prospective buyers and companies in the industry look to beef up their capabilities, investors in the sector tell GCV.

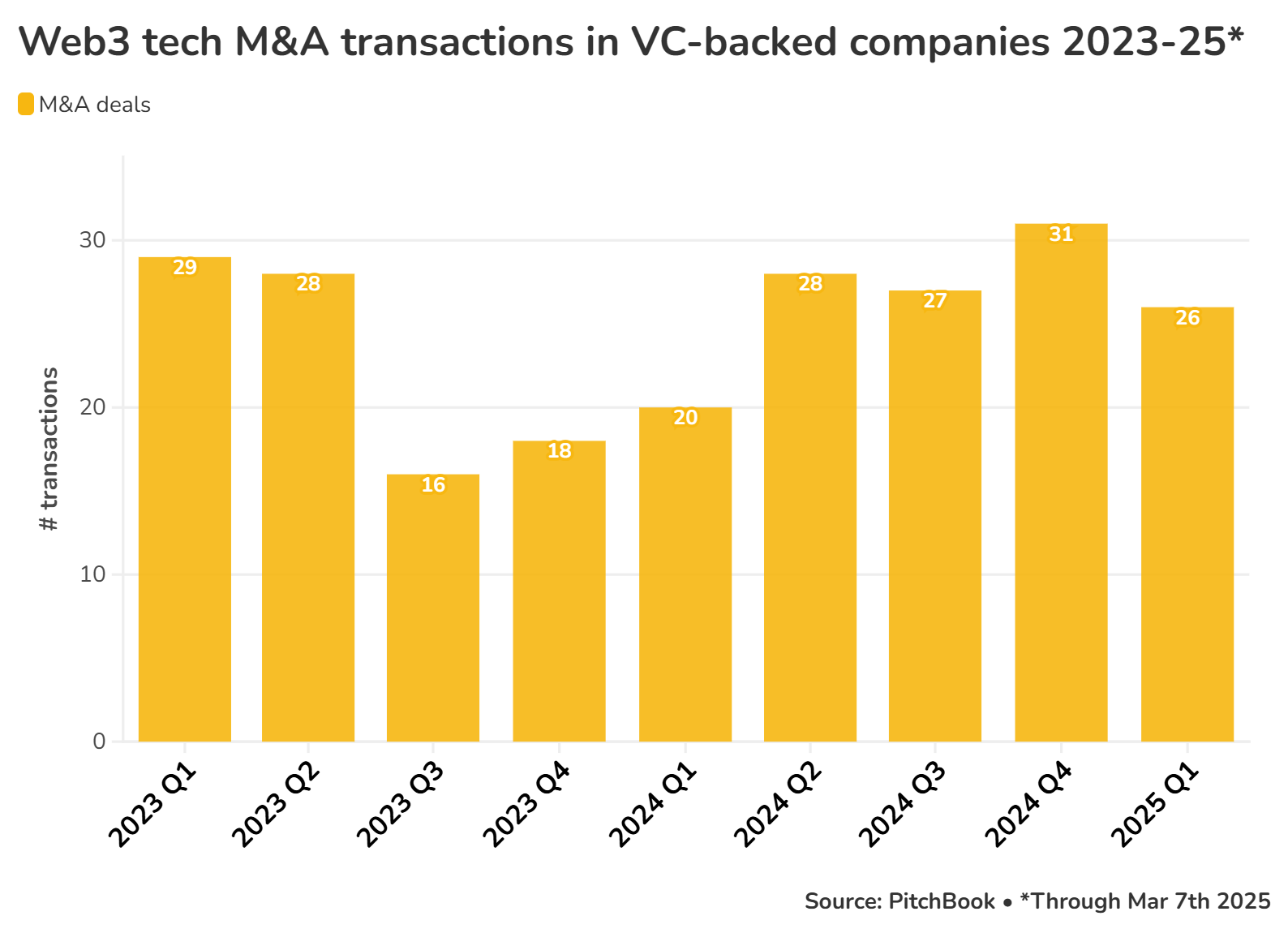

There have been more than two dozen acquisitons already this year including Solana-backed blockchain payment processor Helio being bought by MoonPay for $175m and Chainalysis’s purchase of crypto fraud detection startup Alterya for $150m. Neither had disclosed more than $10m in funding pre-acquisition.

Miko Matsumura, managing partner at blockchain venture fund Gumi Cryptos Capital, sees the Web3 sector as ripe for “high-multiple” M&A due to the new US administration’s embrace of cryptocurrency, which has involved appointing venture capitalist David Sacks as ‘crypto czar’ and plans to create a crypto reserve fund. Both of those moves give the sector credibility and encourage larger organisations to become involved.

“The thing about M&A is that the question becomes about things like mass adoption and regulatory clarity, which enables larger actors to come into the mix,” he says. “Because, if there is not regulatory clarity then there isn’t really an enterprise use.”

Crypto has been an area regulators haven’t wanted to touch, Matsumura adds. And because it’s been regarded as toxic, so far there hasn’t been the effort inside large companies to enter the industry in a substantial way.

“All of the enterprises, all of the boards are going to be asking: what’s our strategy? Why aren’t we doing this? And why are we so far behind?”

Miko Matsumura, Gumi Cryptos Capital

“But if…it reaches the level of a kind of cultural phenomenon, at that point all of the enterprises, all of the boards are going to be asking: what’s our strategy? Why aren’t we doing this? And why are we so far behind?

“I think at that point it becomes a game of catch up. And if they’re trying to catch up, those are the ideal conditions for high-multiple M&A – large players with lots of cash that are kind of desperate to have a play and kind of in a position where they don’t have anything. That’s the perfect storm. And then they start buying at a premium.”

Gakim Solomons, a member of the investment team at financial services firm Standard Chartered’s SC Ventures unit, also sees M&A activity increasing in Web3, a sector largely populated by businesses that began in one part of the market, but which now have to expand their services just to stay competitive. Different pieces of the value chain are getting linked together, he says.

Solomons points to Coinbase as an example of how that value chain works. Coinbase began as a cryptocurrency exchange but now offers asset management and over-the-counter trading services for clients, and is also the custodian of investment giant BlackRock’s exchange traded Bitcoin fund.

Coinbase can run the cryptocurrency custodial services far more cheaply because they are subsidised by the other parts of the company’s business, and that ends up pricing out smaller competitors. It’s an environment that’s primed for consolidation, and Solomons says SC Ventures is seeing that with its own asset book.

“Vertical and horizontal integration is going to happen because of price competition in the market, or because some players cannot get to scale”

Gakim Solomons, SC Ventures

“Vertical and horizontal integration is going to happen because of price competition in the market, or because some players cannot get to scale in that respect, and they won’t be able to effectively grow their businesses, either regionally or globally,” he explains.

“We’re seeing a lot of that at the moment, on the low-margin end of the value chain…parts of the value chain are effectively beginning to come together, so that you are effectively getting a bigger share of the unit economics or a bigger share of the customer wallet.”

That consolidation is why Solomons sees the acquirers mostly coming from within the Web3 market, where traditional players are going to be buying startups elsewhere in that value chain or merging with competitors.

But there will also be large businesses from markets like banking that want to acquire certain blockchain or crypto capabilities, and will do so because it’s open season for them to step into the space.

“There will definitely be acquisitions that take place because it would accelerate their time to market,” he says.

“You’ll probably have a wave of that taking place over the next year. But the consolidation wave is a much bigger wave than banks and asset managers wanting to make acquisitions [to increase their] speed to market.”

The next crop of strategic Web3 investors could come from the entertainment industry

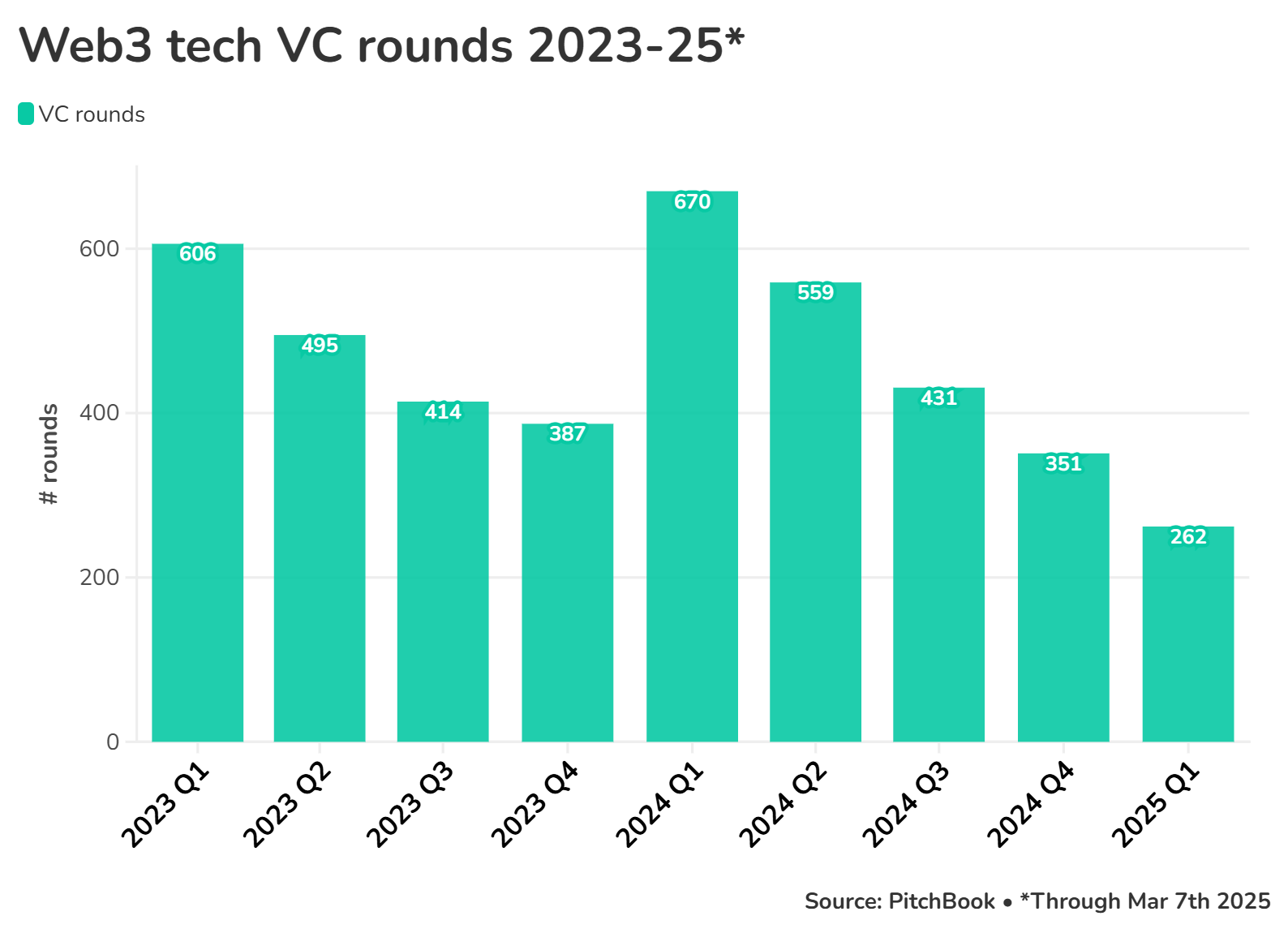

The overall number of startup funding rounds has declined in the past year, as the graph below shows. But this could be changing, says Solomons, as “there has been a lot more activity” for Web3 startups over the past six months, charged by the prospect of a changing regulatory environment and a change of sentiment, particularly in the US, that also pushed Bitcoin past the $100,000 mark in December.

“That sentiment change, and some of the regulatory provisions changing, has just opened the door significantly,” he says. “And we’re seeing that in terms of deal flow. We’re seeing that in terms of clients reaching out to our ventures and our portfolio companies in the space. It’s been quite significant in terms of the groundswell.”

The types of strategic investors are also starting to shift. Much of the venture capital for Web3 startups has traditionally come from within the ecosystem – crypto exchanges like Coinbase and Binance as well as blockchain gaming company Animoca Brands and a slew of specialist funds. But Matsumura says he’s seeing interest coming from a “pioneer species” of larger firms that are beginning to get heavily involved.

“You’re seeing…these really heavy traditional investment firms coming in. You’re seeing things like Sony Corporation with blockchain, and you’re starting to see gaming now,”

Miko Matsumura, Gumi Cryptos Capital

“You’re definitely seeing folks like Franklin Templeton, Brevan Howard, Nomura’s Laser Digital, these really heavy traditional investment firms coming in. You’re seeing things like Sony Corporation with blockchain, and you’re starting to see gaming now,” he says.

Web3 has traditionally been linked with finance, but the technology could also be used with the huge library of movies, TV shows, music or games owned by large entertainment companies. It represents an opportunity to monetise intellectual property (IP) through channels like in-game finance or character-based NFTs.

Sony is involved to the extent it has formed its own public blockchain, Soneium, creating a space where users can potentially build their own applications and digital experiences around its IP. There’s a reason why Austin Noronha, who heads the US arm of Sony’s Innovation Fund, told GCV in December he sees Web3 as one of the key startup trends this year.

The trend is also generational. Generation Alpha, loosely defined as anyone born after 2010, is gravitating towards gamified virtual environments with their own payment systems, like Minecraft and Roblox, and the same kind of metaverse structure is being used in blockchain-based world-building games like The Sandbox. But as this sector progresses, older generations are going to find their own routes in, based on characters and entertainment they already enjoy.

“Everybody wants access to content, to games, to entertainment, but they’re doing it with parties that are familiar to them, unless you have certain breakout-type experiences that occur on a sort of on-and-off basis,” Solomons says.

Much as it has on the financial side, Web3 is also consolidating on the consumer side, with online communities forming around platforms like game-focused Animoca or the Telegram messaging app, says Solomons. There is an opportunity for Web3 companies to expand the services they offer the users on these platforms.

“Developers are building gaming and other consumer applications in these ecosystems,” Solomons says. “And then the token, whether it’s a stablecoin token or a native token, starts to move within this ecosystem as a form of payment for the developers from the consumers to enjoy those gaming experiences.” This offers an opportunity for banking CVC units like SC Ventures, he adds.

“We’ve decided, as our first stage, to basically build and invest in infrastructure. And we are now getting to a point where we are getting into products and services, to not only service corporate clients and institutions, but also to be able to service the Web3 communities. And we’ve started to make a fairly significant inroad into that space today.”

Robert Lavine

Robert Lavine is special features editor for Global Venturing.