Large life sciences deals and corporate investors buying the companies in their own portfolio have been key to an improving exit market.

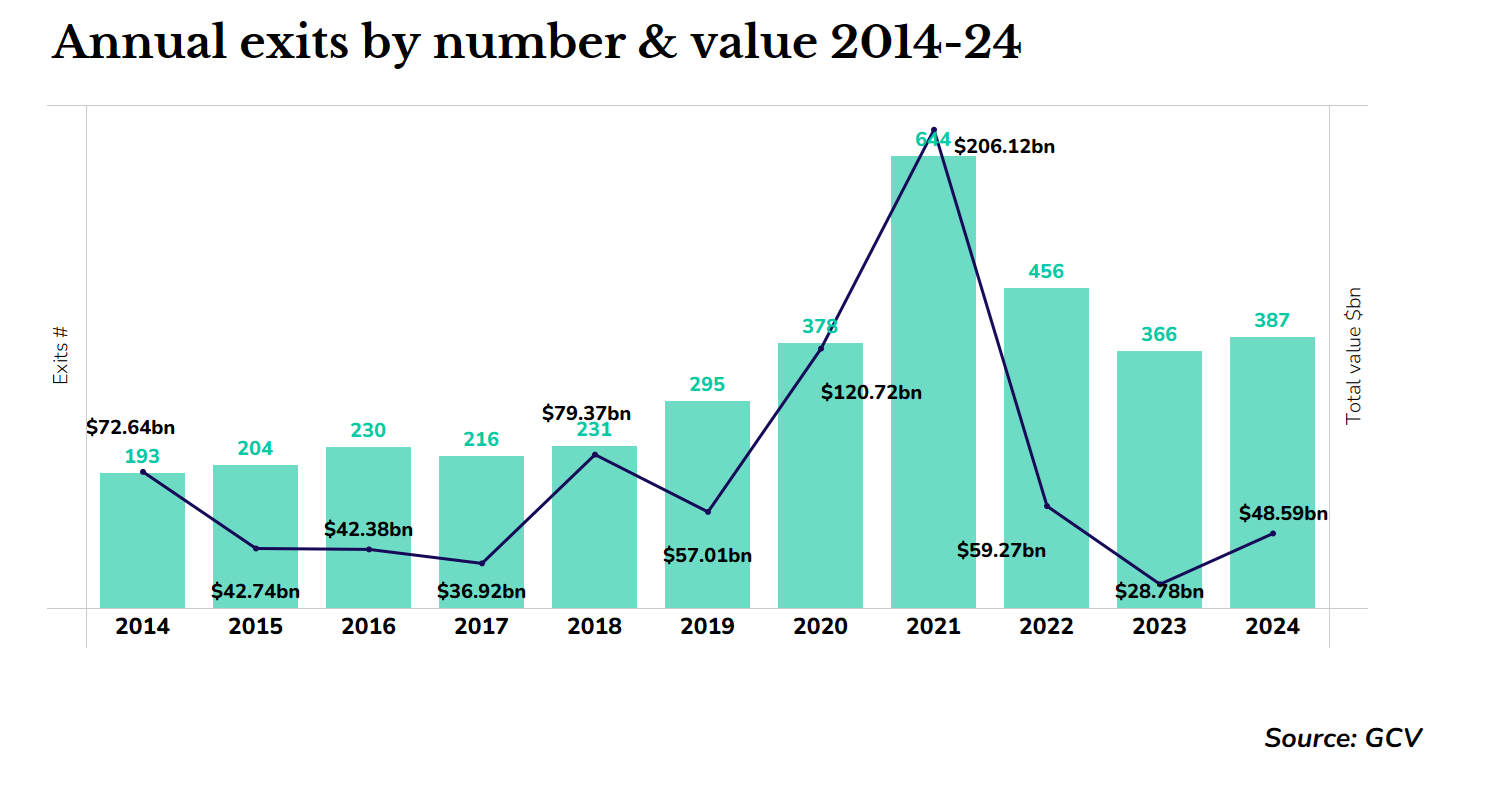

The exit market for corporate-backed startups started to show signs of a pick-up in 2024. The number of exits, at 387, was up 5.7% from the previous year. This is still dramatically lower than the peak seen in 2021, but the value of exits is starting to rise for the first time in two years.

The increase may be partly down to a number of corporations buying companies in their investment portfolio — something that has been relatively rare historically. Private equity firms, too, have also been increasingly willing to buy out stakes from early investors. The life sciences sector, typically an early indicator of an improving exit market, has seen a majority of the largest deals.

The total estimated dollar value of exits for corporate-backed startups was $48.59bn in 2024, up 69% year-on-year versus the $28.78bn registered in 2023.

Most notably, all of the top 10 transactions in 2024 stood above $1bn. Most of the exits came from the life sciences areas but insurance, real estate, cybersecurity and e-commerce also featured large exits.

Corporate parents acquiring portfolio companies

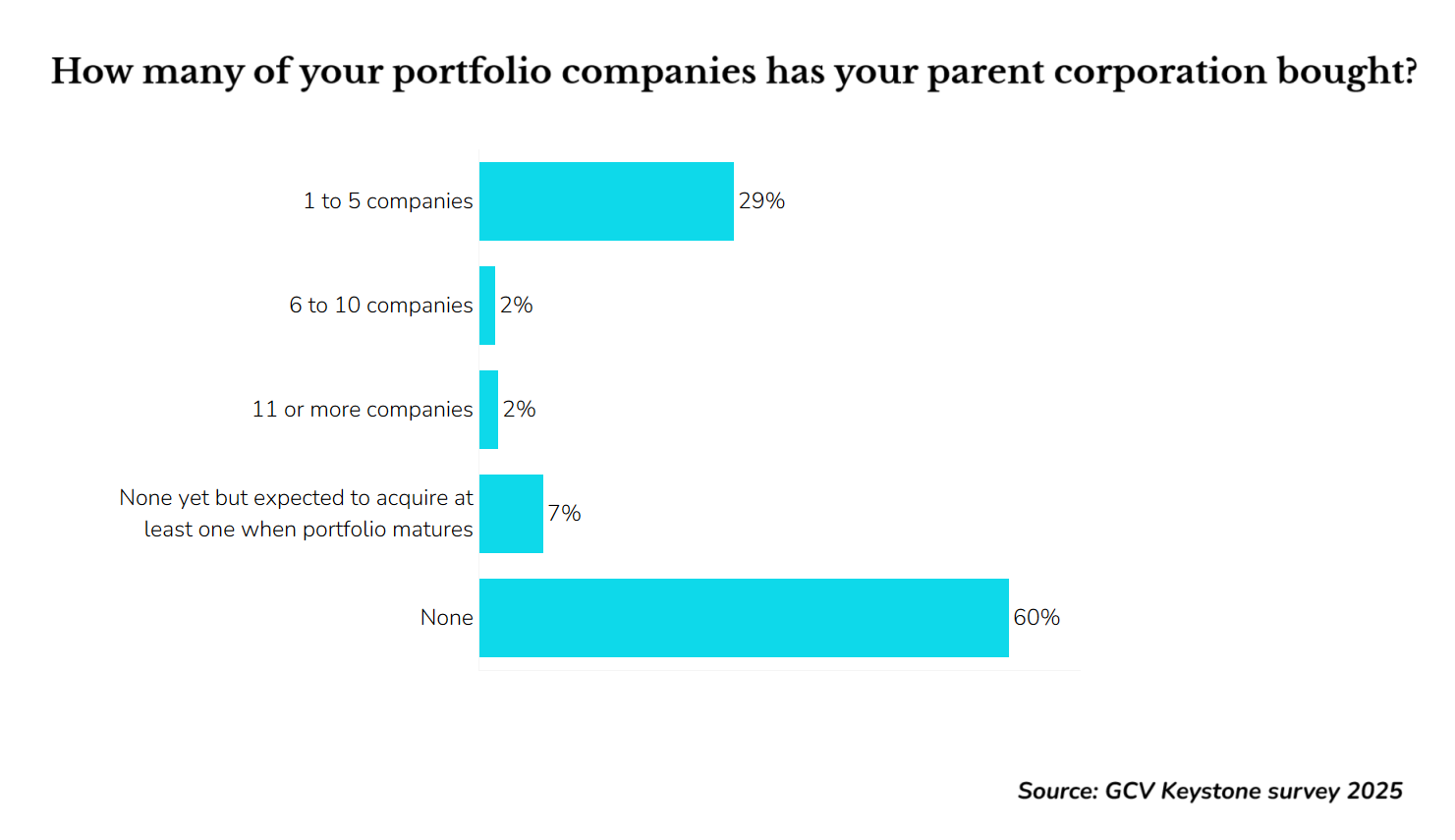

Three of the largest acquisitions we saw in 2024 were instances of acquisitions of the portfolio companies in which the CVC arm of the corporate acquirer had previously taken a minority stake.

Historically, acquisitons like this have been relatively rare. In our annual GCV Keystone annual benchmarking survey, for example, 60% of corporate venturing units report that their parent corporation has never purchased any of the portfolio companies.

One of the biggest acquisitions in 2024, was the purchase of Bermuda-based Resolution Life by Nippon Life Insurance. The Japanese insurance company paid $8.2bn for the remaining 77% of Resolution Life it didn’t already own, valuing the company at $10.6bn. Nippon Life had backed Resolution from 2019, gradually increasing its stake.

The transaction was part of a strategic corporate move within Nippon Life’s strategy to expand internationally amid a saturated domestic market. Founded in 2018, Resolution Life specialises in acquiring and managing closed life insurance books, currently overseeing $85bn in assets and serving 4.3 million policyholders.

Salesforce announced the acquisition of Own Company for $1.9bn in cash. Founded in 2015, Own Company offers cloud data backup and disaster recovery. Before the acquisition, the company reportedly raised over $500m from investors (according to PitchBook), including Salesforce Ventures, Sapphire Ventures and Tiger Global, among others. The acquisition is expected to strengthen Salesforce’s data security offerings.

Merck, known as MSD outside the US and Canada, agreed to acquire EyeBio for $1.8bn, including an upfront payment of $1.3bn. Merck was among the previous backers of the company through its MRL Ventures Fund. Founded in 2021, EyeBio develops therapies for retinal diseases, including its lead candidate, which targets diabetic macular edema and neovascular age-related macular degeneration. The acquisition is expected to bolster Merck’s ophthalmology portfolio and its commitment to addressing unmet needs in retinal health.

Pharma companies (of all sizes) snap up life sciences startups

EyeBio was only one of the large acquisitions of corporate-backed life sciences companies in 2024.

US pharmaceutical company AbbVie agreed to buy Aliada Therapeutics for $1.4bn. Aliada is developing therapeutics designed to treat central nervous system diseases. The company has previously raised venture funding from three corporate VCs- Johnson & Johnson Innovation – JJDC, Sanofi Ventures and OrbiMed. Aliada had raised $53m in venture funding before the acquisition, according to PitchBook’s data.

Biogen entered into a definitive agreement to acquire Human Immunology Biosciences (HI-Bio) for up to $1.8bn. The deal included an upfront payment of $1.15bn with potential additional payments of $650m contingent on development milestones. Founded in 2021, HI-Bio focuses on therapies for immune-mediated diseases, with its lead candidate felzartamab targeting conditions like antibody-mediated rejection in kidney transplants. The acquisition aligns with Biogen’s strategy to expand its immunology and rare diseases portfolio. HI-Bio counted MorphoSys, the biotech developer of therapies against cancer and automune diseases.

Large acquisitions aren’t rare in the life sciences sector but, in 2024, there was also a trend, noted by the Wall Street Journal, of smaller pharmaceutical companies pursuing acquisitions of biotech startups.

We saw one instance of such an acquisition in our top exits for 2024. Clinical-stage biotech ProfoundBio was acquired by Danish biotechnology company Genmab for $1.8bn. ProfoundBio is a clinical-stage biotech firm developing antibody-drug conjugates (ADCs) for cancer treatment. Founded in 2020, ProfoundBio has raised approximately $250m in funding from various investors, including Eli Lilly’s Lilly Ventures Asia back in 2021. This strategic acquisition enhances Genmab’s access to innovative ADC technologies that complement its existing antibody platforms. The integration of ProfoundBio’s assets is expected to broaden Genmab’s clinical pipeline and strengthen its position in the oncology market.

Sluggish IPO markets

In contrast to the pick up in large acquisitions, the IPO market remained sluggish with just one stock market listing for a corporate-backed startup raising more than $1bn.

Swiggy, India’s leading food and grocery delivery platform, debuted on the Indian stock exchanges in November. Its shares opened at ₹420 ($4.93) a 7.7% premium over the IPO price of ₹390 ($4.58), valuing the company at roughly $12bn.

Founded in 2014, Swiggy had previously raised $3.6bn from investors, according to PitchBook. Swiggy managed to raise $1.34bn in the flotation, making it one of India’s largest this year. Its previous backers included multiple corporates like SoftBank, Naspers, Tencent, Meituan, Smile Group and Samsung.

The rise of buyouts

Buyouts by private equity firms have become a key exit strategy for VC-backed companies, with private equity firms stepping in and using their ample capital to acquire startups and offer liquidity to early investors. This approach has been especially prominent in sectors like life sciences, delivering notable capital returns per deal.

London-based private equity firm Cinven acquired a 70% stake in Idealista, an online real estate classifieds platform, operating in Spain, Italy, and Portugal, for $3.10bn, reportedly at a lower valuation than previous funding rounds had valued the company. The company was previously majority-owned by private equity firm EQT, which had acquired its stake in 2020. The portal was previously backed by Spanish banks Caixa Catalunya and Bilbao Bizkaia Kutxa (BBK).

Private equity firm Permira acquired a majority stake in BioCatch, an Israeli company specialising in behavioural biometrics for fraud detection, in a leveraged buy out at a $1.3bn valuation. Founded in 2011, BioCatch uses behavioural analysis to secure over 190 financial institutions globally. The investment aims to accelerate BioCatch’s product innovation and expansion, reflecting the increasing demand for digital fraud prevention solutions. It counted Barclays, Citi Ventures and Amex Ventures among its backers.

Private equity firm Vista Equity Partners made a majority stake investment in Nasuni, a Boston-based enterprise data platform provider, valuing the company at $1.2bn. Founded in 2009, Nasuni specialises in hybrid cloud storage and data management for enterprises. Backed by KKR and TCV, Nasuni serves 850+ clients globally, with the investment aimed at fuelling innovation and international growth. Nasuni counted Dell among its previous backers.

Looking ahead, industry experts anticipate a potential rebound in exits by the end of 2025, driven by expected interest rate cuts and increased political stability, now that the outcome of the US elections has become clear.

Kaloyan Andonov

Kaloyan Andonov is head of analytics at Global Corporate Venturing.