As the AI race dramatically expands energy demand, there has been a palpable shift away from net zero and towards speed and abundance of supply.

The energy sector in 2026 will be shaped by the massive, unprecedented explosion in energy demand in advanced economies as a result of the AI race.

In the three decades between 1990 and 2020, increases in energy demand in OECD countries rarely ventured past 1% in aggregate. But in 2024 demand grow increased to 2.2% and is expected to keep on this faster trajectory.

Businesses have been accelerating their efforts to adjust. In the past year Big Tech has increasingly put capital behind securing its energy supply, with companies like Meta, Google and Amazon investing more money in various types of baseload energy projects to power its data centres.

There has been a palpable shift away from net zero and towards an abundance of energy. The last half-decade’s emphasis on sourcing clean energy has given way to an urgency for more. The time pressure is real and there is a sense that for a nation to win the AI race, it will also have to solve the problem of energy supply.

“The mandate has now changed to: I need to win.”

Alejandro Solé, TechEnergy Ventures

”Where I see the risk is, are we able to put all the pieces together in a timeframe that everyone wants? Is there a real national strategic advantage in winning the AI race? Because to do that, you need all this infrastructure, and to have all of this infrastructure, you need all these pieces to come together,” says Pradeep Tagare, head of investments at National Grid Partners.

“Fundamentally, it’s hard to get all these pieces to come together in an accelerated timeframe. That’s the challenge.”

Need to win

“The priorities are clearer now. It’s speed first, cost second, clean third,” says Alejandro Solé, chief investment officer at TechEnergy Ventures, the VC arm of industrial conglomerate Techint Group’s energy division, Tecpetrol.

AI has changed the calculus for the large energy customers in tech. Whereas five years ago, tech companies were tripping over themselves to sign renewable power purchase agreements to shore up their green bona fides, they now care far less how green it is.

“The mandate has now changed to: I need to win,” says Solé.

“The velocity and pragmatism with which the world has refocused on this topic has been surprising. There are a lot of good energy startups that, if they’re not at the centre of AI, it’s as if no one is interested, even if they have a lot to offer.”

On the upswing

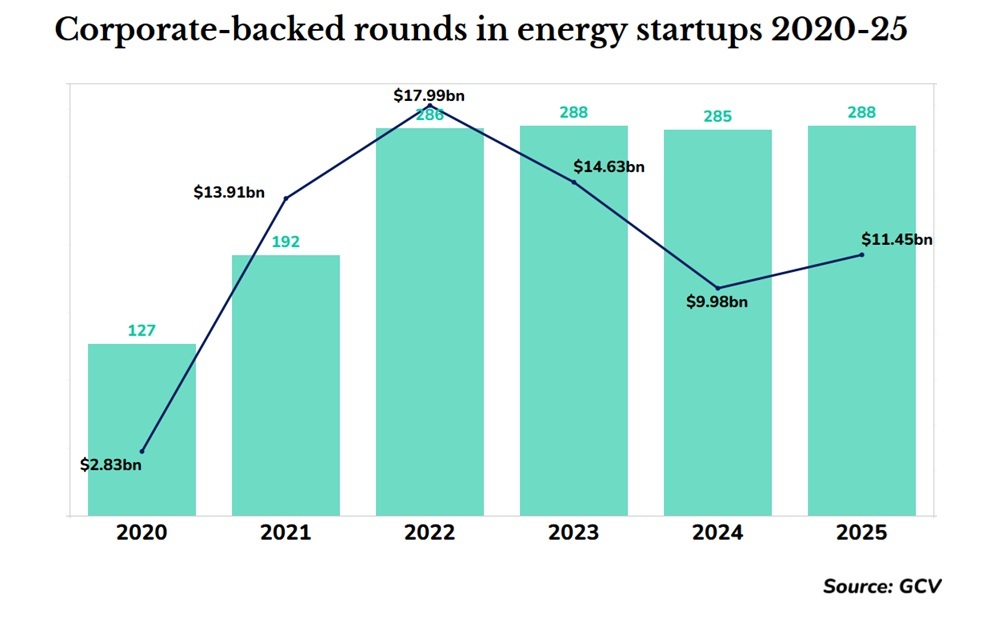

In terms of venture deal flow, the energy sector was famously unique in its resiliency through the venture downturn, with the number of corporate-backed funding rounds relatively constant even as they dipped in other sectors.

The dollars invested in corporate-backed funding rounds, however, have declined since 2022, until this past year saw a small rebound, according to GCV data.

Up to mid-December, 2025 has had a nearly identical number of funding rounds as the past three years, but up nearly $1.5bn in capital invested compared to 2024, signalling larger rounds on average.

There were modest decreases in sub-segments like renewable energy and energy storage, but increases for technologies like energy software and analytics, and grid and power supply technologies.

Decarbonisation to abundance

Between 2024 and 2030, data centres’ aggregate demand for power is expected to roughly double from 415TWh to 945TWh, accounting for just under 3% of the world’s total energy demand, before rising to 1,200TWh by 2035, according to the International Energy Agency. To the extent that the developed world sees AI as determinative of economic dominance, it does not get there without sorting the energy issue.

To that end, the scale of the demand spike is such that there will be no one-size-fits-all solution – it will take a kaleidoscope of technology beyond the generative ones that are already well-established.

“Bring your own capacity” has been embraced as a principle for those building and operating data centres, and while clean energy is ideal, companies are largely agnostic about the source – natural gas, behind-the-meter renewables or energy storage, nuclear, geothermal, or anything else available.

Read GCV’s Energy Report on the challenge posed by data centre demand

Optimising the use of existing grid assets will also be a huge growth area as new infrastructure build-outs of transmission assets will be far slower than the demand for power.

At the same time, a range of technologies – geothermal, nuclear, next-generation conduction materials, energy efficiency and load management systems and more – are evolving or being trialled, and it remains too early to tell which will come out on top.

“I think 2026 is the year when we will have data from a bunch of these approaches and that puzzle will start to, I don’t think get fully solved next year, but I think we’ll have very good data exiting 2026 on which ones of these can potentially scale,” says Tagare.

What will likely see even less interest over the next year are any purely “green” or “net zero-focused” technologies that take more power than they generate. Carbon capture is one of the more emblematic technologies here, with very few concrete and bankable solutions on the horizon, still requiring high capex and not often energy-generative, it has been hard for it to move as a technology.

Hydrogen, too, continues to go through an adjustment in terms of how people see it fitting into the energy matrix. Whereas five years ago it was seen a potential energy source, now the view is shifting more to having it as a clean feedstock for chemicals or steel.

Funding and exits

The exit landscape in 2025 has markedly improved across the venture capital industry, and the signs have also been encouraging in the energy space, but it is not quite there yet. Next year, investors hope, it will open up more.

“We are cautiously optimistic that 2026, the initial M&A trend will continue. We are seeing that across our portfolio – there are three or four discussions going on as we speak, so that is encouraging. We do expect that the IPO window will start to open next year,” says Tagare.

On the funding side, says Tagare, it will be interesting to see the extent to which many of the cleantech funds that were formed in the 2020-2021 boom cycle will be able raise substantial capital for early stage decarbonisation plays.

“I think that will largely determine where the eventual funding goes, whether it goes to early stage or if it will likely shift to more mid-stage and growth stage.”

Track all the corporate investments in energy startups in the

CVC Funding Round Database

Fernando Moncada Rivera

Fernando Moncada Rivera is a reporter at Global Corporate Venturing and also host of the CVC Unplugged podcast.