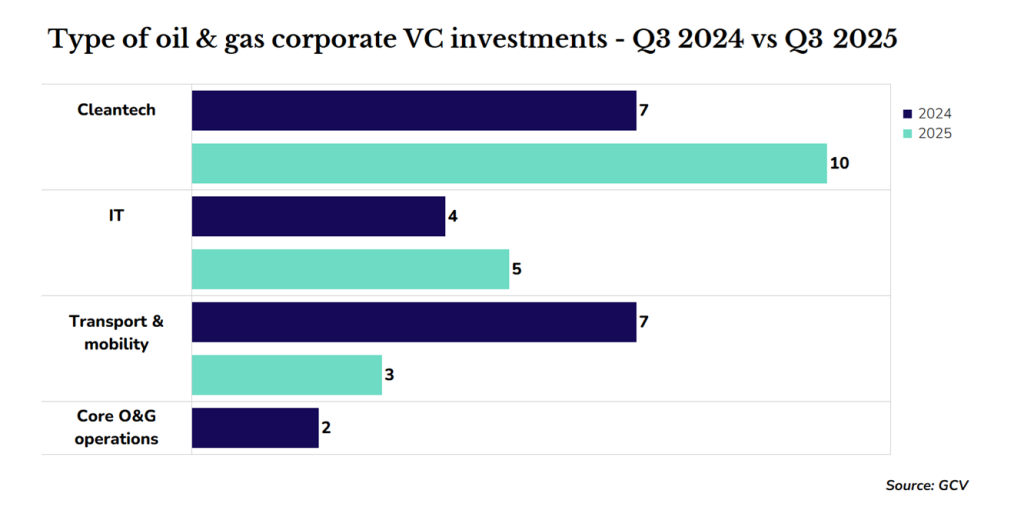

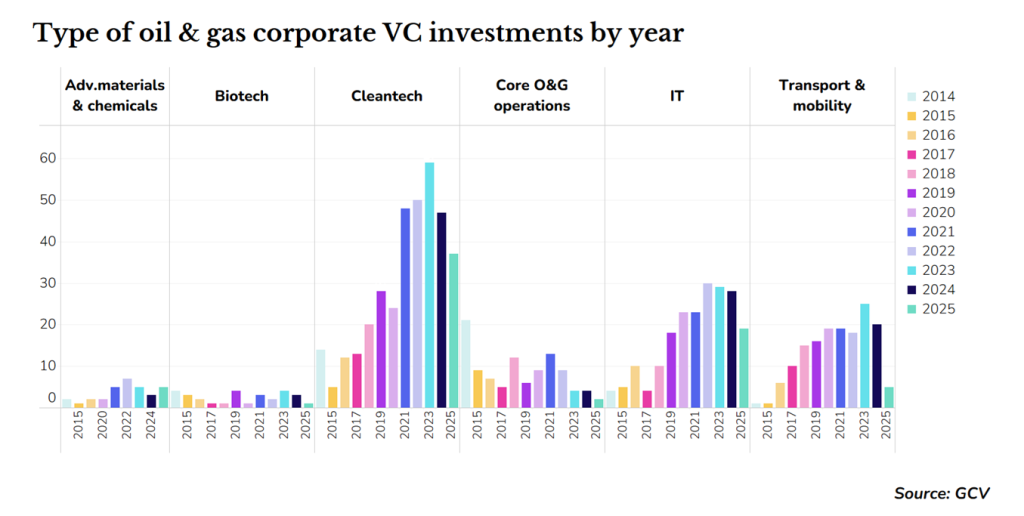

Cleantech and IT remain the main focus for corporates, with fusion and hydrogen taking a big role.

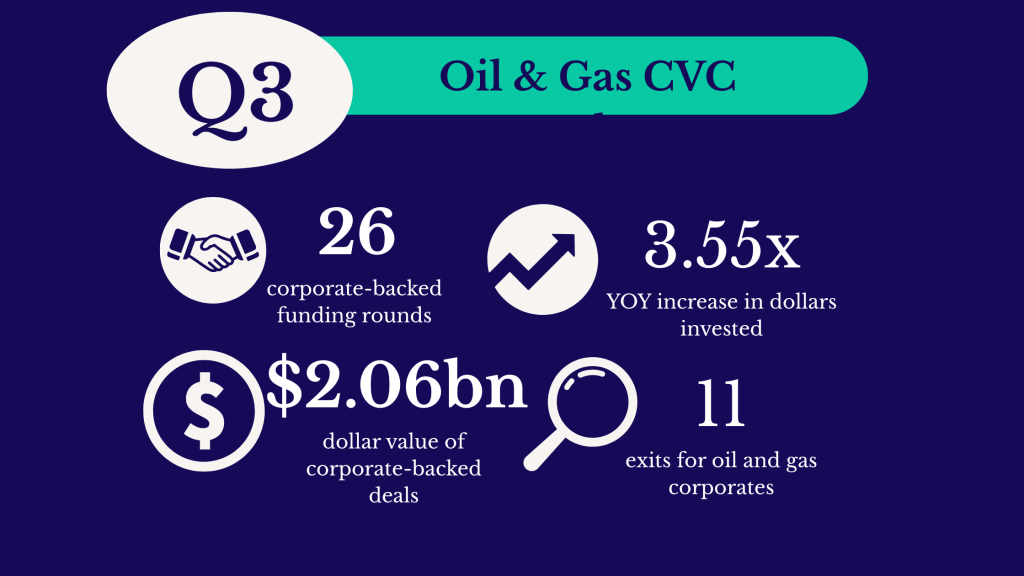

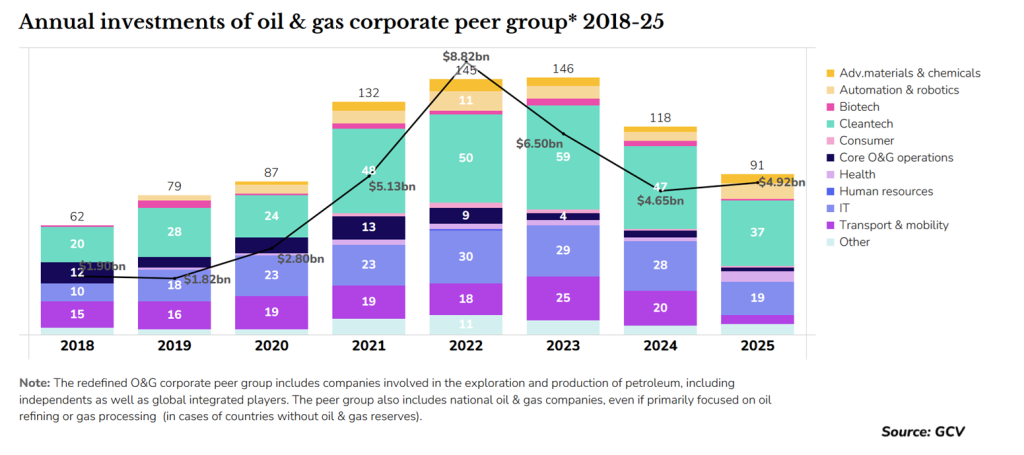

Venture spending by oil and gas companies in Q3 was dominated by one big fusion deal – the $1.6bn round for China Fusion Energy, which brought the total dollars invested to $2.06bn.

With the China Fusion Energy deal, the total disclosed amount raised in rounds was more than triple the number of venture capital dollars spent in the third quarter of last year. Without that one outlier, however, we see one of the lowest amounts of disclosed dollars invested in the past few years.

The oil and gas report is part of of GCV’s quarterly update on energy sector trends.

Fusion has been a big theme for investors over recent months, especially in the APAC region, where Japan’s Helical Fusion raised a $15.6m series A round and Linea Innovation, also in Japan, raised $12.2m. In the US, Commonwealth Fusion raised a $863m round from investors including Jera, Japan’s largest power company, Kansai Electric Power, and Mitsui OSK Lines, the transport company.

While these recent fusion funding rounds did not include investors from oil and gas companies, earlier in the year Chevron Technology Ventures backed the $150m funding round for fusion startup TAE Technologies, and Chevron and Shell Ventures both backed fusion company Zap Energy at the end of last year.

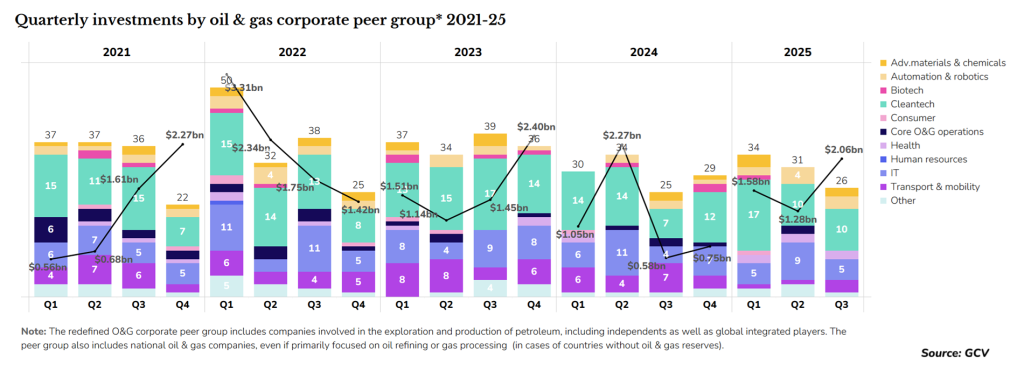

Overall, cleantech is, as ever, the biggest single segment drawing venture investment from oil majors, with IT still holding its usual second-place spot. Some of the bigger cleantech deals include a $47m Equinor-backed series B for Lithium de France which is developing environmentally-friendly lithium extraction and a $28m series B round for sustainable aviation fuel company OXCCU that was backed by Saudi Aramco and Eni Group.

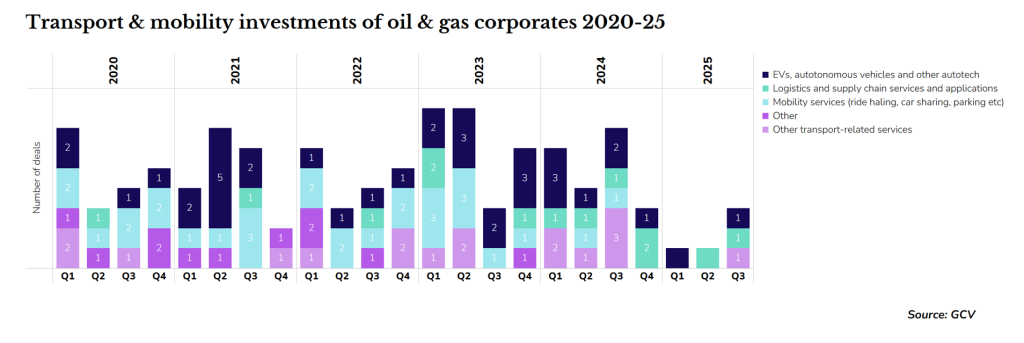

Transport and mobility, which usually gets several investments every quarter from the big oil companies, has fallen off in 2025, with no quarter seeing more than three rounds in the sector.

So far this year, most subsectors are down from the year before in terms of number of oil and gas company-backed rounds, with the exception of advanced materials and chemicals.

Startups like Radical AI, the AI-aided advanced materials developer that raised a $55m round, backed by Eni Group along with corporates like Nvidia and Raytheon Technologies, showcases AI’s continued inroads into every subsector. Meanwhile India’s deep tech materials developer Chakr Innovation also got an investment from the likes of Oil and Natural Gas Corporation.

Cleantech and IT are both on track to potentially surpass last year’s numbers if the fourth quarter continues current trends.

See how your corporate venture unit compares against global norms and best practice by taking our annual benchmarking survey.

- All answers anonymised.

- All participants receive a free copy of the benchmarking report.

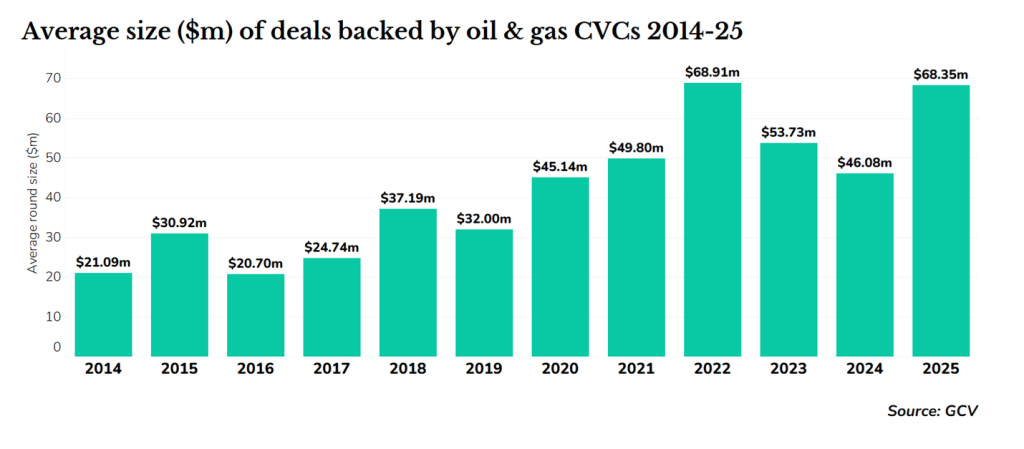

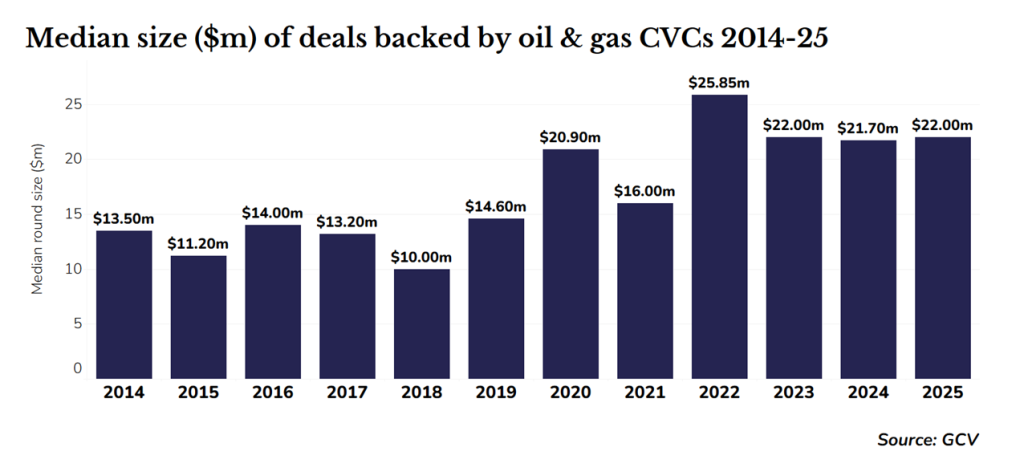

The average size of a funding round involving oil and gas investors has been falling since 2022. The China Fusion Energy deal somewhat misleadingly pushed the averages up for 2025, to $68.35m. However, taking out the outliers, the median round size is similar to the previous two years.

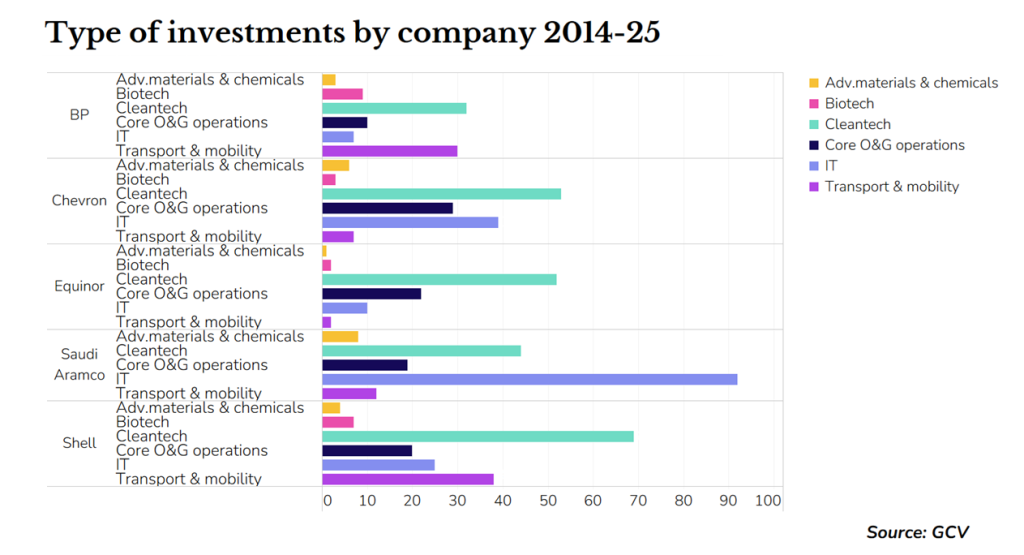

Over the past decade, cleantech has been the single biggest investment sector for many of the oil and gas majors. One notable exception has been Saudi Aramco, which has invested in twice as many rounds in IT than in cleantech as it has worked to digitise and modernise its systems.

Shell and BP, both of which have made big bets on electric vehicle charging infrastructure, have transport and mobility as their second biggest investment target since 2014, though BPs investment is the smallest of these major players at it has slowed down its activity over the past year or so.

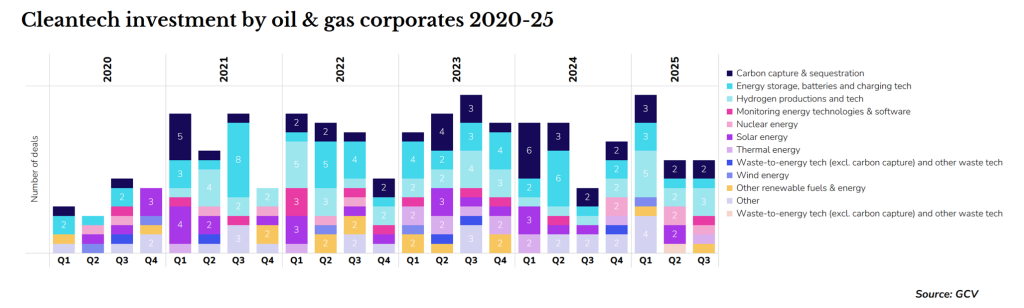

Within the cleantech space, oil and gas corporates seem to have rediscovered their interest in hydrogen, with Q3 2025 seeing as many hydrogen investments by the peer group as there had been up to the same point last year.

Investment in startups such as hydrogen and natural gas recovery systems developer Sapphire Technologies’ Equinor-backed $18m series C, as well as the Woodside Energy-backed $7m seed round for electrolyser manufacturer Stargate Technologies, have pushed up the numbers. Energy sector investments in hydrogen are on track to surpass any year since at least 2020 if this trend continues.

On the other hand, carbon capture and energy storage, which both saw a lot of activity over the past two years, have seen their deal numbers go down in 2025.

Transport startups seem to have had the biggest fall from favour among oil and gas corporates. Despite having three times as many rounds as in the first or second quarters of 2025, Q3 still has as few transport rounds as any quarter since Q4 2021.

Transport may have seen weak investment numbers, but it had one of the biggest exits of the quarter, when public mobility platform provider Via went public in a $493m IPO, providing exits for Shell, alongside other corporates including Bank Hapaolim, Hearst, Koch Industries and Daimler.

Fernando Moncada Rivera

Fernando Moncada Rivera is a reporter at Global Corporate Venturing and also host of the CVC Unplugged podcast.