Corporate investors can add real value to startup boards but it is crucial to have the right person with the right training in the seat, and to understand how to navigate conflicts of interest well.

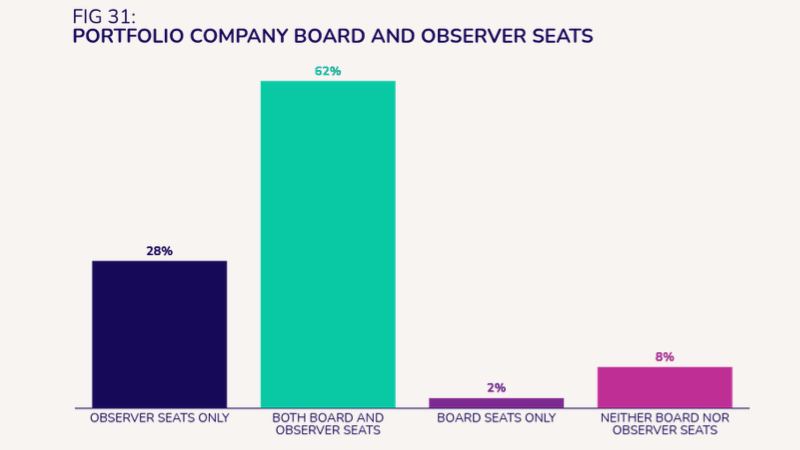

Corporate venture capital is expanding with around one in every five startup funding rounds now including a corporate backer. Those companies in general want and expect to take board seats at the startups they invest in, either as observers or as full, voting members. GCV’s latest annual benchmarking survey shows that some 92% of corporate investment units will take some type of position on the board of a portfolio company.

Corporate investors have always wanted to have some kind of representation on the board, says Luca Gori, partner and co-head of emerging growth companies and venture capital at DLA Piper, “because they’re not solely interested in the financial return, but whether they can learn something. So they have always asked for it.”

The difference now, he says, is that “there’s more acceptance from the portfolio companies, and more understanding of the value that a corporate venture can actually bring to the table.”

Previously, startups tended pushed back against the idea of corporate representatives sitting on their boards. Now it is more likely that they welcome it as a way of building deeper relationships with a company that may become a key go-to-market business partner or customer.

Corporate investors must, however, ensure that those board positions really do benefit the startup, avoid potential conflicts and genuinely add value rather than simply increasing complexity.

In a recent webinar John Glushik, managing director of HG Ventures, the corporate venture arm of The Heritage Group, and Martin Cheski, partner and investment director at Telus Global Ventures, the investment arm of Canadian technology company Telus, joined Gori to outline six lessons that maximise the effectiveness of board seats on both sides.

1. Decide who should take the seat

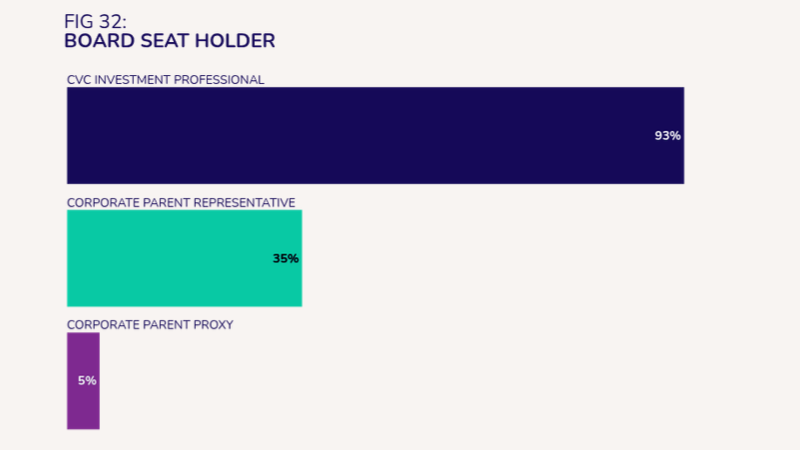

The first decision is not whether to take a board role but who in the corporate should occupy it. It is more common for a member of the corporate venture team to take this role — this is the case for 93% of the companies polled in our recent annual benchmarking survey. A further 35% of companies appoint a business unit leader to a board role.

Opinions on whether it is better for board seats to go to CVCs or business unit members can be sharply divided. At HG Ventures, Glushik’s team always allocates the board seat to a member of the venture group. He says that investment professionals are best equipped to deal with the responsibilities and fiduciary duties of the role.

At Telus Global Ventures, the approach is more varied. Cheski explains that the company would typically begin with a venture investor as a board member. “We typically start with one of our investment team members that joins the board. They work with the board for six to 12 months. And then at that time, we determine if this board seat better off to stay with the CVC unit, or is it appropriate for our business unit counterparty to interact.”

The underlying principle is that the identity of the board representative should follow the value-creation strategy not the other way around. The more the investment is about joint go‑to‑market and deeply strategic alignment, the stronger the case for involving a business unit leader – provided they are properly trained and understand their duties.

2. Understand the difference between a board member and observer role

The distinction between a voting board member and an observer is not cosmetic. As Gori puts it:

“There is a significant difference between the two. The board is subject to duties that are generally set out in some code in whichever country you are being appointed as a board member, whilst the observer, if it’s true to its name, should just be observing. Maybe [they] can speak, but don’t vote, don’t direct the company, and don’t have any duties to the company other than possibly some confidentiality duties.”

Glushik underlined the fiduciary dimension:

“If you’re a board member and you have potential conflicts, you’re going to have to manage those conflicts because you do have a duty, and in some cases, there’s legal consequences. So it is a meaningful difference.”

For corporates, this means that opting for an observer seat can reduce complexity where conflicts are likely, or where the corporate’s contribution is primarily advisory and network-based rather than governance-driven.

Yet, as Cheski pointed out, observers do not have to be passive:

“I would encourage that you take a more active, participatory role, rather than a true I’m just going to attend a meeting, take the information, and, you know, not help kind of move the company forward.”

3. Preparation and training is crucial

A board seat is not a trophy; it is a workload and a responsibility. Individually, board participants must invest the time. Gori warns that being overstretched across too many companies is a liability:

“If you are on 30 portfolio companies, are you really reading 30 board packs from the first page to the last? Those questions have been probed in courts of law,” he says. “If you really haven’t been doing much, you lose all of the benefits of being a board member, but you still keep all of the potential liabilities of having breached your duty.”

From the corporate side, training is not optional. Cheski described Telus’ approach:

“Most of our corporate venture teams are trained on what it means to be a board member, what it means to be a good member, good observer; the business units potentially less so. So I would encourage everyone to have a some sort of training programme.”

That training is then tailored further:

“We also run an internal training programme that says, Okay, you understand how to operate as a board member in a general sense. Now, for our particular sense, these are the things that you need to be aware of.”

Structurally, firms such as Telus also embed board practices internally:

“We’ll discuss those in our partners meetings. We’ll do downloads of here’s what happened at the board meeting at a high level, here’s the challenges that they’re facing. You really need to learn from others, and it will be a journey.”

For startups, the implication is clear: insist that corporate board participants are trained, resourced and backed by a clear internal process not acting as isolated emissaries.

The GCV Institute runs board member training courses four times a year. Details about the next course here.

4. Manage conflicts of interest

Conflicts between the interests of a startup and those of a large corporate parent are not hypothetical; they are structural.

“There are situations where something that is for the benefit of the portfolio company may not be for the benefit of the corporate venture that appointed you – when the company is going through a refinancing, when the company is in difficult situation, when they are competing for the same type of contract with the government,” says Gori.

In such cases, process matters as much as intent. Glushik is blunt:

“Good intentions are not enough. Having a structural process in place is critical to make sure that those conflicts are managed very intentionally.”

This may involve recusal, abstaining from votes, carefully managing information flows between business units and the venture arm, or – in extreme cases – resignation from the board.

Cheski argues that the starting point should be clear legal guidance and boundaries. One of them centres on information flows and making sure confidentiality is respected.

“We don’t issue statements to our business unit counterparts without the approval of the company. We don’t issue product roadmaps. We don’t discuss that. So we have very curated conversations,” says Cheski. “I think you need to build that level of respect with the portfolio company, that you know you will keep their confidential information confidential.”

Consulting a lawyer might be a good place to start.

“The CVC unit needs to get legal advice on the boundaries and guidelines they need to follow and operate because it does expose the company, as well as the individual, to legal liability if they’re not followed.”

For founders, this underlines the importance of negotiating and documenting conflict‑management mechanisms early, rather than relying on personal rapport or verbal assurances.

5. How corporates board members add value and where they can hurt

Despite the risks of corporate board participation, when done well it can be a valuable asset. Cheski describes how Telus uses even small stakes and observer roles to bring about progress:

“Sometimes we’ll act as the catalyst in that situation, where we’ll bring the board together, will help support in camera conversations, will lead a consortium of some of the board members. And then the other area is you’re the trusted advisor of some of the board members.”

He also highlights the value of bringing corporate functional expertise directly into committees:

“Rather than one of our venture partners taking the board seat, we put one of our VPs of finance from Telus on that particular board seat [and] we were able to help that company rapidly and efficiently scale their finance function.”

Glushik says HG Ventures’ entire strategy is focused on value-add:

“We focus on investing in companies where we can help. So, our focus is adding value, and that value is typically delivered through the expertise on our team and the great domain expertise and technical expertise we have across the Heritage Group.”

Yet, there is a downside when corporates mis-manage the role. Excessive turnover of board representatives undermines trust and continuity.

“One of the knocks against corporate venture taking a board seat is that there’s turnover. We see that within our teams, people in the CVC unit sometimes come and go. So it swaps out board roles, and that creates some concerns for founders,” says Cheski.

In short, corporates can bring credibility, networks, operational know‑how and strategic alignment – but only if they commit for the long term, invest in governance competence, and treat the board seat as a duty not an option.

6. The need to take board roles seriously

Corporate board seats have become much more common at startups, and are much more accepted by founders than a decade ago.

That acceptance, however, is not automatic licence. It carries with it heightened expectations of professionalism, transparency and discipline. For corporates, failing to prepare their board representatives properly exposes both the startup and the parent company to real governance and legal risk. For startups, failing to interrogate who sits in the seat and under what terms risk inviting a powerful yet conflicted actor into the room where the most consequential decisions are made.

Both sides, in other words, have strong incentives to make this conversation far more deliberate than it has often been to date.

Watch the full webinar replay below:

This webinar is part of GCV’s The Next Wave series. We run webinars monthly on different areas of corporate investment practice. Our next webinar will be: “Venture Clienting: A smarter path to innovation — or a strategic distraction?” on April 22, 2026. Secure your place on the webinar here.

Maija Palmer

Maija Palmer is editor of Global Venturing and puts together the weekly email newsletter (sign up here for free).